Kinross reports strong 2026 first-quarter results

Rhea-AI Summary

Kinross (TSX: K, NYSE: KGC) reported first-quarter results for the period ended March 31, 2026.

The company delivered record free cash flow for the fourth consecutive quarter, reported margins that continued to outpace the gold price, and returned approximately $350 million to shareholders year-to-date in 2026 (and $1 billion since Q1 2025). The company also reported significant progress across its pipeline of development projects.

AI-generated analysis. Not financial advice.

Positive

- Record free cash flow for the fourth consecutive quarter

- Margins continuing to outpace the gold price

- Returned approximately $350 million to shareholders in 2026

- Total shareholder returns of $1 billion since Q1 2025

- Significant progress across development project pipeline

Negative

- None.

News Market Reaction – KGC

On the day this news was published, KGC gained 1.27%, reflecting a mild positive market reaction. Argus tracked a peak move of +3.3% during that session. Our momentum scanner triggered 15 alerts that day, indicating notable trading interest and price volatility. This price movement added approximately $448M to the company's valuation, bringing the market cap to $35.76B at that time.

Data tracked by StockTitan Argus on the day of publication.

Key Figures

Peers on Argus

KGC fell 5.04% while key gold/precious peers like AU (-0.64%), FNV (-1.08%), PAAS (-0.56%), WPM (-1.91%), and AGI (-1.69%) saw more modest declines. The move appears more company-specific than sector-driven.

Historical Context

| Date | Event | Sentiment | Move | Catalyst |

|---|---|---|---|---|

| Apr 10 | Mini-tender warning | Neutral | -0.6% | Company advised shareholders to reject below-market mini-tender offer. |

| Apr 01 | Earnings date set | Neutral | -1.6% | Announced timing for Q1 2026 release, call, and annual meeting. |

| Mar 19 | Buyback renewal | Positive | -3.2% | Renewed NCIB to repurchase up to 104,239,211 common shares. |

| Mar 03 | Trade show update | Neutral | -8.1% | Korea Ginseng Corporation promoted products at an industry expo. |

| Feb 18 | Dividend increase | Positive | -3.2% | Announced 14% annual dividend increase to $0.16 per share. |

Recent Kinross headlines, including shareholder returns and buybacks, have often been followed by short-term negative price reactions, indicating a tendency for the stock to trade down around ostensibly shareholder-friendly news.

Over the last six months, Kinross has focused on capital returns and corporate housekeeping. It renewed its NCIB on March 19, 2026 to repurchase up to 104,239,211 shares and announced a 14% annual dividend increase to $0.16 per share with a Q4 2025 dividend of $0.04. The company also issued administrative updates on reporting calendars and urged investors to reject a below-market mini-tender offer. Despite generally supportive news, shares often traded lower following these announcements.

Regulatory & Risk Context

Market Pulse Summary

This announcement highlights Kinross’s focus on cash generation and shareholder returns, with record free cash flow for the 4th consecutive quarter and about $350 million returned in 2026, totaling $1 billion since Q1 2025. In recent months, the company has also renewed its share repurchase program and raised its annual dividend. Investors may watch subsequent disclosures for more detail on margins, project execution, and whether this level of cash generation and capital return can be maintained alongside growth initiatives.

AI-generated analysis. Not financial advice.

Delivered record free cash flow for the 4th consecutive quarter, margins continued to outpace gold price

Returned approximately

Significant progress across pipeline of development projects

TORONTO, April 29, 2026 (GLOBE NEWSWIRE) -- Kinross Gold Corporation (TSX: K, NYSE: KGC) (“Kinross” or the “Company”) today announced its results for the first quarter ended March 31, 2026.

This news release contains forward-looking information about expected future events and financial and operating performance of the Company. We refer to the risks and assumptions set out in our Cautionary Statement on Forward-Looking Information located on pages 24 and 25 of this release. All dollar amounts are expressed in U.S. dollars, unless otherwise noted.

2026 first-quarter highlights:

- Production1 of 492,563 gold equivalent ounces (Au eq. oz.).

- Production cost of sales2 of

$1,397 per Au eq. oz. sold and attributable production cost of sales1 of$1,380 per Au eq. oz. sold. - Attributable all-in sustaining cost1 of

$1,732 per Au eq. oz. sold. - Operating cash flow3 of

$1,139.5 million . - Record attributable free cash flow1 of

$837.5 million . - Margins4 increased by

92% compared with Q1 2025 to a record$3,476 per Au eq. oz. sold, and increased by22% quarter-over-quarter, outpacing the rise in the average realized gold price in both comparable periods. - Reported earnings5 of

$843 million , or$0.70 per share, with adjusted net earnings6 of$854.1 million , or$0.71 per share. - On track to meet annual guidance: On an attributable basis1, Kinross expects to produce 2.0 million Au eq. oz. (+/-

5% ) at a production cost of sales per Au eq. oz. sold1 of$1,360 (+/-5% ) and all-in sustaining cost1 of$1,730 (+/-5% ) per ounce sold for 2026. Total attributable capital expenditures1 are forecast to be$1,500 million (+/-5% ). - Cash and cash equivalents increased to

$2.2 billion , and the Company has total liquidity7 of approximately$3.9 billion at March 31, 2026.

Return of capital to shareholders:

- Kinross is on track to return

40% of its free cash flow to shareholders in 2026. During the first quarter, the Company repurchased approximately$250 million in shares, and an additional$50 million in April. - Including its quarterly dividend, Kinross has returned approximately

$350 million in capital to shareholders to date as of April 29, 2026. - Between April 2025 and March 31, 2026, Kinross returned over

$1 billion of capital to shareholders and reduced its share count by more than3% . - Kinross’ Board of Directors declared a quarterly dividend of

$0.04 per common share payable on June 4, 2026, to shareholders of record at the close of business on May 21, 2026.

Operations:

- Paracatu was the strongest contributor in the portfolio and achieved record recoveries reflecting the results of a sustained, multi-front optimization program across the processing plant including further optimisation of the gravity gold recovery circuit within the grinding circuit.

- Tasiast continued to perform well, with higher production supported by higher grades and lower cost of sales per ounce sold compared with the previous quarter.

Development projects:

- Great Bear’s Advanced Exploration (“AEX”) program is well advanced with surface construction approximately

90% complete and all permits received. At the Main Project, detailed engineering is45% complete, and the third and final phase of the Impact Statement was submitted during the quarter, as planned. - Lobo-Marte’s Environmental Impact Assessment was submitted in April 2026 and is under review by the regulators, formally initiating the permitting process.

- Round Mountain Phase X underground development is progressing well and is slightly ahead of schedule. The project received its final permit, marking the completion of all major operational permitting.

- At Kettle River-Curlew (“Curlew”), early works were completed, underground development is ahead of schedule, and key site infrastructure continues to advance.

- At Bald Mountain Redbird, project execution continued to advance. Mining is ongoing, the vertical carbon-in-column plant is nearing completion, earthworks for the heap leach pad extension are well ahead of schedule, and procurement and engineering for the SART plant are progressing on plan.

Sustainability:

- Consistent with Kinross’ commitment to responsible mining, its 2025 Sustainability Report is expected to be published during the second quarter, marking its 18th edition. The report will provide a comprehensive summary of Company performance over the past year and outline Sustainability priorities.

CEO commentary:

J. Paul Rollinson, CEO, made the following comments in relation to 2026 first-quarter results:

“Kinross delivered another excellent quarter. We generated record free cash flow of approximately

“We have returned approximately

“In the current situation of global uncertainty, we continue to benefit from an attractive relative cost position, supported by our longstanding approach to mitigate cost pressures. This includes the hedging of fuel and currency exposures as well as the continued execution of our grade enhancement strategy. Both are proving effective in the current environment of elevated oil prices and differentiate Kinross.

“In Q1, our pipeline of high-quality development projects advanced on plan. At Great Bear, we continued to make strong progress across both Advanced Exploration and the Main Project. Engineering and procurement are advancing as planned, and new exploration results further reinforce the scale and long-term potential of the deposit.

“At Lobo-Marte, the submission of the Environmental Impact Assessment in April marked an important milestone, formally initiating the permitting process for this long-life, large-scale growth project. Our new U.S. projects – Round Mountain Phase X, Curlew and Redbird – made steady progress and remain firmly on track. Also, we are continuing our studies on our significant resource inventory as we target additional potential mine life extensions across our portfolio.”

Summary of financial and operating results

| Three months ended | ||||||

| March 31, | ||||||

| (in millions of U.S. dollars, except ounces, per share amounts, and per ounce amounts) | 2026 | 2025 | ||||

| Operating Highlights(a) | ||||||

| Total gold equivalent ounces(b) | ||||||

| Produced | 500,941 | 529,861 | ||||

| Sold | 494,128 | 524,089 | ||||

| Attributable gold equivalent ounces(b) | ||||||

| Produced | 492,563 | 512,088 | ||||

| Sold | 485,855 | 506,564 | ||||

| Gold ounces - sold | 482,472 | 516,268 | ||||

| Silver ounces - sold (000's) | 674 | 701 | ||||

| Earnings(a) | ||||||

| Metal sales | $ | 2,407.7 | $ | 1,497.5 | ||

| Production cost of sales | $ | 690.5 | $ | 546.7 | ||

| Depreciation, depletion and amortization | $ | 275.7 | $ | 288.4 | ||

| Operating earnings | $ | 1,338.1 | $ | 570.4 | ||

| Net earnings attributable to common shareholders | $ | 843.0 | $ | 368.0 | ||

| Net earnings per share attributable to common shareholders (basic and diluted) | $ | 0.70 | $ | 0.30 | ||

| Adjusted net earnings(c) | $ | 854.1 | $ | 364.0 | ||

| Adjusted net earnings per share(c) | $ | 0.71 | $ | 0.30 | ||

| Cash Flow(a) | ||||||

| Net cash flow provided from operating activities | $ | 1,139.5 | $ | 607.1 | ||

| Attributable adjusted operating cash flow(c) | $ | 1,129.3 | $ | 620.3 | ||

| Capital expenditures(d) | $ | 283.2 | $ | 207.7 | ||

| Attributable capital expenditures(c) | $ | 278.9 | $ | 204.1 | ||

| Attributable free cash flow(c) | $ | 837.5 | $ | 380.8 | ||

| Per Ounce Metrics(a) | ||||||

| Average realized gold price per ounce(e) | $ | 4,873 | $ | 2,857 | ||

| Attributable average realized gold price per ounce(c) | $ | 4,873 | $ | 2,856 | ||

| Production cost of sales per equivalent ounce sold(b)(f) | $ | 1,397 | $ | 1,043 | ||

| Attributable production cost of sales per equivalent ounce sold(b)(c) | $ | 1,380 | $ | 1,038 | ||

| Attributable production cost of sales per ounce sold on a by-product basis(c) | $ | 1,296 | $ | 1,010 | ||

| Attributable all-in sustaining cost per equivalent ounce sold(b)(c) | $ | 1,732 | $ | 1,355 | ||

| Attributable all-in sustaining cost per ounce sold on a by-product basis(c) | $ | 1,657 | $ | 1,331 | ||

| Attributable all-in cost per equivalent ounce sold(b)(c) | $ | 2,199 | $ | 1,678 | ||

| Attributable all-in cost per ounce sold on a by-product basis(c) | $ | 2,135 | $ | 1,660 | ||

| (a) | All measures and ratios include |

| (b) | “Gold equivalent ounces” include silver ounces produced and sold converted to a gold equivalent based on a ratio of the average spot market prices for the commodities for each period. The ratio for the first quarter of 2026 was 57.79:1 (first quarter of 2025 – 89.69:1). |

| (c) | The definition and reconciliation of these non-GAAP financial measures and ratios is included on pages 17 to 23 of this news release. Non-GAAP financial measures and ratios have no standardized meaning under IFRS and therefore, may not be comparable to similar measures presented by other issuers. |

| (d) | “Capital expenditures” is “Additions to property, plant and equipment” on the interim condensed consolidated statements of cash flows. |

| (e) | “Average realized gold price per ounce” is defined as gold revenue divided by total gold ounces sold. |

| (f) | “Production cost of sales per equivalent ounce sold” is defined as production cost of sales divided by total gold equivalent ounces sold. |

The following operating and financial results are based on first-quarter gold equivalent production:

Production: Kinross produced 492,563 Au eq. oz. in Q1 2026, compared with 512,088 Au eq. oz. in Q1 2025, a decrease of

Average realized gold price8: During the quarter, the average realized gold price was

Revenue: Revenue increased to

Production cost of sales: Production cost of sales per Au eq. oz. sold2 increased to

Attributable production cost of sales per Au oz. sold on a by-product basis1 was

Margins4: Kinross’ margin per Au eq. oz. sold increased by

Attributable all-in sustaining cost1: Attributable all-in sustaining cost per Au eq. oz. sold was

In the first quarter, attributable all-in sustaining cost per Au oz. sold on a by-product basis was

Operating cash flow3: Operating cash flow was

Attributable adjusted operating cash flow1 for Q1 2026 was

Attributable free cash flow1: Attributable free cash flow more than doubled to

Reported net earnings5: Reported net earnings more than doubled to

Adjusted net earnings6 more than doubled to

Reported net earnings and adjusted net earnings in Q1 2026 included

Capital expenditures9: Capital expenditures increased to

Attributable capital expenditures1 were

Balance sheet

Kinross added approximately

The Company had additional available credit10 of

Return of capital to shareholders

Kinross’ 2026 buyback strategy is on track. The Company plans to allocate

Kinross repurchased approximately

As part of its quarterly dividend program, the Company also declared a dividend of

Outlook

The following section of the news release represents forward-looking information and users are cautioned that actual results may vary. We refer to the risks and assumptions contained in the Cautionary Statement on Forward-Looking Information on pages 24 and 25 of this news release.

Kinross remains on track to deliver its 2026 annual guidance for production, cost of sales per ounce, all-in sustaining cost and capital expenditures. Kinross also remains on track to achieve its Effective Tax Rate (ETR) guidance with a lower expected ETR from Q2 2026 to Q4 2026, and on track to meet its full-year taxes paid guidance. Due in part to Kinross’ ongoing hedging programs, cost impacts of rising crude oil prices beginning in March 2026 have been minimal and are not expected to affect the Company’s ability to achieve its full-year cost guidance.

To better reflect global market conditions and the potential impacts of elevated oil prices, Kinross is providing more detail on its oil price sensitivity11 for its full-year guidance in the table below.

| Impact on cost of sales per ounce per | Summary | Impact on full-year guidance of a | |

| 2026 oil sensitivity12 | Direct impacts of crude oil on refined fuel products | ||

| 2026 sensitivity related to refining, distribution and taxes | Includes refining, distribution and taxes | ||

| Total fuel cost sensitivity | (~ | ||

| Potential additional secondary cost sensitivity | + ~ | Considers potential secondary impacts related to freight and other consumables | + ~ (~ |

Operating results

Mine-by-mine summaries for 2026 first-quarter operating results may be found on pages 11 and 15 of this news release. Highlights include the following:

At Tasiast, quarter-over-quarter production increased, driven by strong grades, and cost of sales per ounce sold decreased. Year-over-year, production was lower primarily due to the timing of ounces processed through the mill, partially offset by higher grades due to planned mine sequencing. Compared with Q1 2025, cost of sales per ounce sold increased primarily due to higher royalties as a result of higher gold prices.

At Paracatu, production increased quarter-over-quarter with record recoveries as a result of a multi-front optimization program across the processing plant, and increased year-over-year due to the improved recoveries as well as the timing of ounces processed through the mill. Cost of sales per ounce sold increased slightly quarter-over-quarter due to higher royalty costs, and increased year-over-year as a result of higher royalty and drilling contractor costs, and strengthening of the Brazilian real.

At La Coipa, production decreased quarter-over-quarter mainly due to lower tonnes processed as a result of a planned mill maintenance shutdown in March and lower grades due to planned mine sequencing. Year-over-year, production increased primarily due to the timing of ounces processed through the mill, partially offset by the decrease in grades, and cost of sales per ounce sold was higher due to increased labour and reagent costs, strengthening of the Chilean peso, and higher royalties.

At Fort Knox, production was higher quarter-over-quarter, with increased cost of sales per ounce sold due to the timing of ounces processed through the mill and heap leach pads. Year-over-year, production decreased primarily due to lower mill grades and recoveries, partially offset by the timing of ounces processed through the mill. Compared with Q1 2025, cost of sales per ounce sold increased primarily due to processing more tonnes at lower grade through the mill as well as timing of ounces recovered.

At Round Mountain, production decreased quarter-over-quarter and year-over-year primarily due to lower-grade, lower-recovery stockpile feed as mining transitions from Phase W to Phase S. Higher-grade, higher-recovery ore from Phase S is expected in the second half of the year. Cost of sales per ounce sold increased in both comparable periods due to the lower production.

At Bald Mountain, production decreased quarter-over-quarter due to the timing of ounces recovered from heap leach pads, and decreased year-over-year due to fewer tonnes placed on the heap leach pads and lower grades. Cost of sales per ounce sold increased quarter-over-quarter due to fewer ounces produced, and increased year-over-year as a result of the lower production and higher royalties.

Development projects

Great Bear

At Great Bear, Kinross continues to progress its AEX program alongside permitting, detailed engineering and procurement of major equipment for the Main Project.

For AEX, construction of the water treatment plant, including mechanical, piping, and electrical work, was substantially complete, with surface construction approximately

Regarding the Main Project, detailed engineering is advanced and is approximately

Main Project permitting continues to advance. Federally, Great Bear submitted the third and final phase of its Impact Statement to the Impact Assessment Agency of Canada in March 2026 as planned. Relevant submissions have also been submitted to Fisheries and Oceans Canada.

Provincially, Great Bear continues to work with the Ontario authorities to advance provincial permitting under the One Project, One Process (“1P1P”) permitting process. The next 1P1P steps are approval of the Project Definition and issuance of an Integrated Authorization and Permitting Plan.

In relation to Lac Seul and Wabauskang First Nations, on whose traditional territory the Great Bear Project resides, we are pleased to report that negotiations on the Impact and Benefits Agreement continue to advance based on a recently signed and confidential Memorandum of Understanding that captures the key economic compensatory and procurement elements.

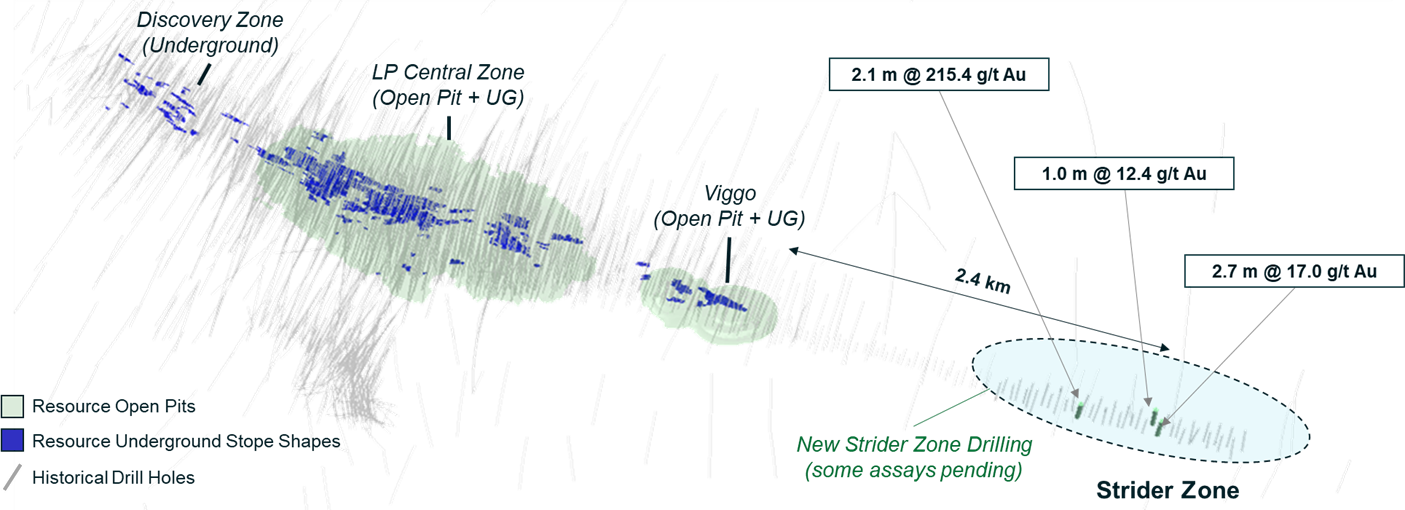

Recent drilling in the new Strider zone has returned mineralized intercepts on trend with the main LP zone, over 2.4 kilometres away from the existing resource. Drilling is ongoing to further test and delineate the structure along strike and at depth.

Highlights include:

- 2.1m @ 215.4 g/t Au

- 1.0m @ 12.4 g/t Au

- 2.7m @ 17.0 g/t Au

Great Bear Plan View:

A photo accompanying this announcement is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/dd58fa8b-ba33-4c3c-82d7-c5786facd287

Lobo-Marte

Lobo-Marte’s Environmental Impact Assessment was submitted in April 2026 and is under review by the regulators, formally initiating the permitting process and marking a milestone for this growth project.

Lobo-Marte is expected to support long-life, large-scale production with the potential to produce approximately 4.7 million gold equivalent ounces over a 16-year mine life14. The project is designed to leverage Kinross’ existing operating experience and infrastructure in Chile.

The Company looks forward to providing a project update in the second half of the year.

Round Mountain Phase X

Underground development at Round Mountain Phase X is progressing well and is slightly ahead of schedule, with over 7,200 metres developed to date. Engineering work is progressing well, site planning for surface and underground infrastructure are well advanced. During the quarter, Kinross marked the completion of all major operational permitting for the Phase X project. Procurement of long lead items including mining equipment is progressing as planned.

Curlew

At Curlew, Kinross progressed key site infrastructure as well as detailed engineering and procurement for the mill refurbishment. The Company has selected a contractor for the mill refurbishment, with mobilization activities beginning. Underground mine development also advanced in Q1 2026 ahead of schedule to de-risk the path to first production in 2028.

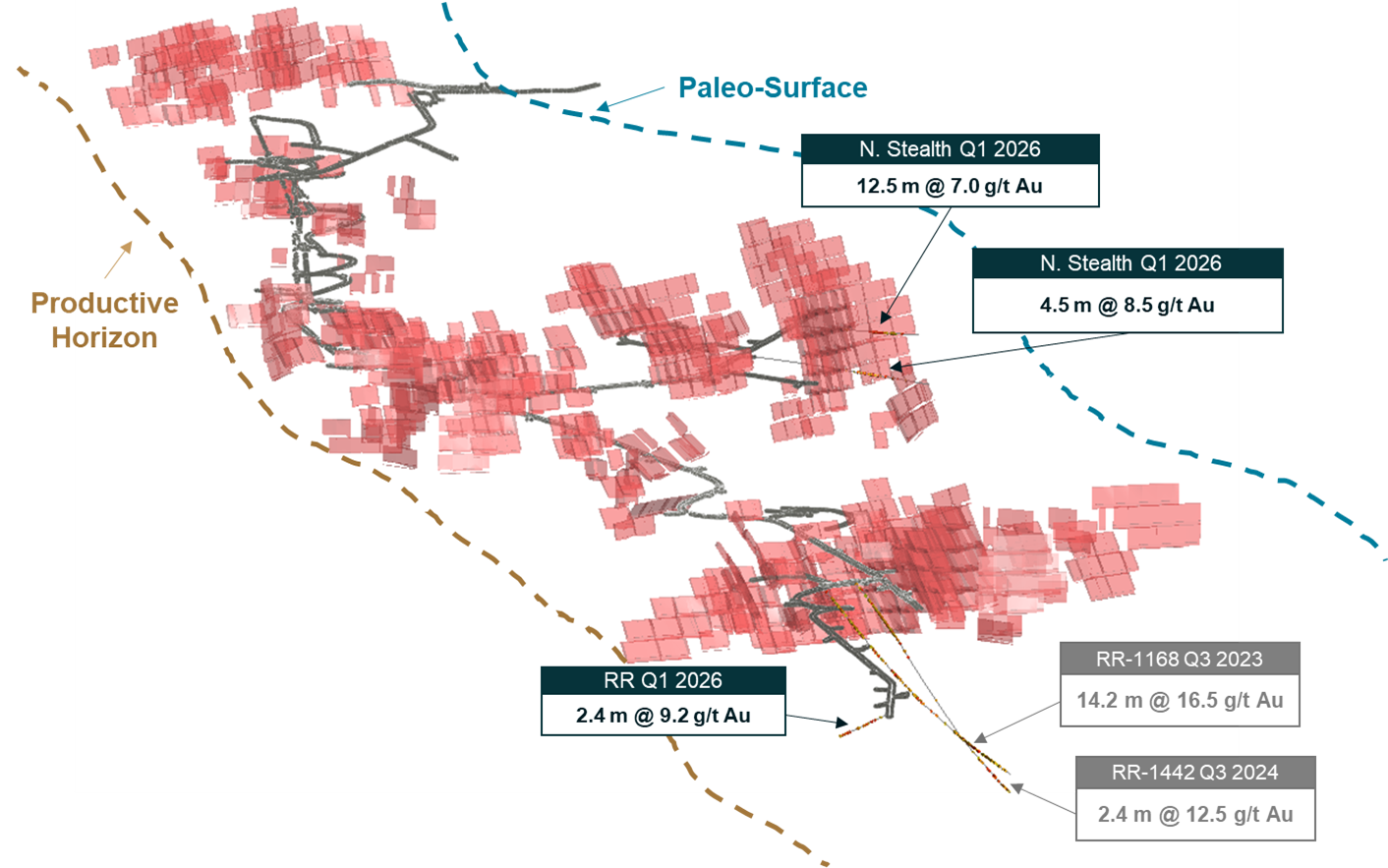

Exploration continued to demonstrate the potential for additional high-grade mineralization with successful drilling at North Stealth and Roadrunner. At North Stealth, recent drilling intersected strong grades and widths, confirming continuity and supporting the extension of mineralization to the east and west. At Roadrunner, drilling continues to return high-grade intercepts, reinforcing the prospectivity of the target area.

Highlights include:

- N. Stealth - 12.5m @ 7.0 g/t Au

- N. Stealth - 4.5m @ 8.5 g/t Au

- RR - 2.4m @ 9.2 g/t Au

Curlew Cross Section:

A photo accompanying this announcement is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/a407cab2-ac71-4075-a17c-68c6984a7785

Bald Mountain Redbird

At Redbird, Kinross continued to advance project execution across several key areas. Mining is ongoing, the construction of processing infrastructure is progressing well, and earthworks for the heap leach pad extension are ahead of schedule, supported by favourable winter conditions. Significant progress was made on the ordering and initial receipt of major mining equipment, and the design and engineering for the SART plant progressed on plan.

Sustainability

Kinross advanced its research partnership with Lakehead University with a five-year funding commitment to support the Northern Ontario Heritage Fund Industrial Research Chair in Mineral Exploration, established with grant funding from the Northern Ontario Heritage Fund Corporation. In addition to supporting exploration efforts at Great Bear, the partnership is expected to play an important role in training and developing the future workforce through graduate students and field assistants, helping build the skilled talent base in the region and create opportunities for local communities.

In Chile, Kinross advanced its commitment to community well-being by partnering with public and private stakeholders to finance the development of a new angiography unit at the Copiapó Regional Hospital. The investment addresses a critical healthcare gap in the Atacama region, which previously lacked access to advanced cardiovascular diagnostic and treatment capabilities, and is expected to improve timely care and health outcomes for thousands of residents.

Kinross plans to publish its 2025 Sustainability Report in the second quarter, providing a transparent account of its Sustainability performance and outlining priorities in the year ahead and beyond.

Conference call details

In connection with this news release, Kinross will hold a conference call and audio webcast on April 30, 2026, at 8:00 a.m. EDT to discuss the results, followed by a question-and-answer session. To access the call, please dial:

Canada & US toll-free – (888) 596-4144; Conference ID: 9425112

Outside of Canada & US – +1 (646) 968-2525; Conference ID: 9425112

Replay (available up to 14 days after the call):

Canada & US toll-free – +1 (800) 770-2030; Conference ID: 9425112 #

Outside of Canada & US – +1 (609) 800-9909; Conference ID: 9425112 #

You may also access the conference call on a listen-only basis via webcast at our website www.kinross.com. The audio webcast will be archived on www.kinross.com.

Annual Meeting of Shareholders

Kinross’ Annual Meeting of Shareholders will be held on Thursday, April 30, 2026, at 10:00 a.m. EDT.

The meeting will be accessible online at: https://meetings.lumiconnect.com/400-541-772-335. The link to the meeting will also be accessible at www.kinross.com and will be archived for later use.

Voting and participation instructions for eligible shareholders are provided in the Company’s Notice of Annual Meeting of Shareholders and Management Information Circular.

This release should be read in conjunction with Kinross’ 2026 first-quarter unaudited Financial Statements and Management’s Discussion and Analysis report at www.kinross.com. Kinross’ 2026 first-quarter Financial Statements and Management’s Discussion and Analysis have been filed with Canadian securities regulators (available at www.sedarplus.ca) and furnished with the U.S. Securities and Exchange Commission (available at www.sec.gov). Kinross shareholders may obtain a copy of the financial statements free of charge upon request to the Company.

About Kinross Gold Corporation

Kinross is a Canadian-based global senior gold mining company with operations and projects in the United States, Brazil, Mauritania, Chile and Canada. Our focus is on delivering value based on the core principles of responsible mining, operational excellence, disciplined growth, and balance sheet strength. Kinross maintains listings on the Toronto Stock Exchange (symbol: K) and the New York Stock Exchange (symbol: KGC).

Media Contact

Samantha Sheffield

Director, Corporate Communications

phone: 416-365-3034

Samantha.Sheffield@Kinross.com

Investor Relations Contact

David Shaver

Executive Vice-President, Investor Relations & Communications

phone: 416-365-2854

InvestorRelations@Kinross.com

Review of operations

| Three months ended March 31, | Gold equivalent ounces | |||||||||||||||||

| Produced | Sold | Production cost of sales ($millions) | Production cost of sales/equivalent ounce sold | |||||||||||||||

| 2026 | 2025 | 2026 | 2025 | 2026 | 2025 | 2026 | 2025 | |||||||||||

| Tasiast | 130,014 | 137,629 | 131,679 | 129,493 | 130.3 | 105.0 | 990 | 811 | ||||||||||

| Paracatu | 160,583 | 146,639 | 158,849 | 146,855 | 177.7 | 139.6 | 1,119 | 951 | ||||||||||

| La Coipa | 54,211 | 52,315 | 53,737 | 55,870 | 82.0 | 64.1 | 1,526 | 1,147 | ||||||||||

| Fort Knox | 102,372 | 112,054 | 96,218 | 112,110 | 174.8 | 131.8 | 1,817 | 1,176 | ||||||||||

| Round Mountain | 26,200 | 35,686 | 26,084 | 35,960 | 72.4 | 57.0 | 2,776 | 1,585 | ||||||||||

| Bald Mountain | 27,561 | 45,538 | 27,561 | 43,801 | 53.3 | 49.2 | 1,934 | 1,123 | ||||||||||

| United States Total | 156,133 | 193,278 | 149,863 | 191,871 | 300.5 | 238.0 | 2,005 | 1,240 | ||||||||||

| Less: Manh Choh non-controlling interest ( | (8,378 | ) | (17,773 | ) | (8,273 | ) | (17,525 | ) | (19.9 | ) | (20.7 | ) | ||||||

| United States Attributable Total | 147,755 | 175,505 | 141,590 | 174,346 | 280.6 | 217.3 | 1,982 | 1,246 | ||||||||||

| Operations Total | 500,941 | 529,861 | 494,128 | 524,089 | 690.5 | 546.7 | 1,397 | 1,043 | ||||||||||

| Attributable Total | 492,563 | 512,088 | 485,855 | 506,564 | 670.6 | 526.0 | 1,380 | 1,038 | ||||||||||

Consolidated balance sheets

| (expressed in millions of U.S. dollars, except share amounts) | |||||||||

| As at | |||||||||

| March 31, | December 31, | ||||||||

| 2026 | 2025 | ||||||||

| Assets | |||||||||

| Current assets | |||||||||

| Cash and cash equivalents | $ | 2,185.0 | $ | 1,742.3 | |||||

| Restricted cash | 15.3 | 13.5 | |||||||

| Accounts receivable and prepaid assets | 129.0 | 145.8 | |||||||

| Inventories | 1,315.2 | 1,370.3 | |||||||

| Other current assets | 30.5 | 16.6 | |||||||

| 3,675.0 | 3,288.5 | ||||||||

| Non-current assets | |||||||||

| Property, plant and equipment | 8,310.0 | 8,289.4 | |||||||

| Long-term investments | 115.7 | 99.3 | |||||||

| Other long-term assets | 769.6 | 708.9 | |||||||

| Deferred tax assets | 13.5 | 25.0 | |||||||

| Total assets | $ | 12,883.8 | $ | 12,411.1 | |||||

| Liabilities | |||||||||

| Current liabilities | |||||||||

| Accounts payable and accrued liabilities | $ | 665.2 | $ | 716.4 | |||||

| Current income tax payable | 543.1 | 595.7 | |||||||

| Current portion of provisions | 75.2 | 74.2 | |||||||

| Other current liabilities | 9.5 | 13.3 | |||||||

| 1,293.0 | 1,399.6 | ||||||||

| Non-current liabilities | |||||||||

| Long-term debt | 738.5 | 738.2 | |||||||

| Provisions | 977.7 | 976.6 | |||||||

| Other long-term liabilities | 51.5 | 64.8 | |||||||

| Deferred tax liabilities | 602.2 | 537.8 | |||||||

| Total liabilities | $ | 3,662.9 | $ | 3,717.0 | |||||

| Equity | |||||||||

| Common shareholders' equity | |||||||||

| Common share capital | $ | 4,363.8 | $ | 4,382.0 | |||||

| Contributed surplus | 9,851.3 | 10,137.6 | |||||||

| Accumulated deficit | (5,148.2 | ) | (5,943.3 | ) | |||||

| Accumulated other comprehensive income (loss) | 31.4 | (0.3 | ) | ||||||

| Total common shareholders' equity | 9,098.3 | 8,576.0 | |||||||

| Non-controlling interests | 122.6 | 118.1 | |||||||

| Total equity | $ | 9,220.9 | $ | 8,694.1 | |||||

| Total liabilities and equity | $ | 12,883.8 | $ | 12,411.1 | |||||

| Common shares | |||||||||

| Authorized | Unlimited | Unlimited | |||||||

| Issued and outstanding | 1,194,109,463 | 1,199,843,037 | |||||||

Consolidated statements of operations

| (expressed in millions of U.S. dollars, except per share amounts) | |||||||||

| Three months ended | |||||||||

| March 31, | March 31, | ||||||||

| 2026 | 2025 | ||||||||

| Revenue | |||||||||

| Metal sales | $ | 2,407.7 | $ | 1,497.5 | |||||

| Cost of sales | |||||||||

| Production cost of sales | 690.5 | 546.7 | |||||||

| Depreciation, depletion and amortization | 275.7 | 288.4 | |||||||

| Total cost of sales | 966.2 | 835.1 | |||||||

| Gross profit | 1,441.5 | 662.4 | |||||||

| Other operating expense | 20.3 | 14.0 | |||||||

| Exploration and business development | 38.2 | 42.3 | |||||||

| General and administrative | 44.9 | 35.7 | |||||||

| Operating earnings | 1,338.1 | 570.4 | |||||||

| Other expense - net | (13.3 | ) | (13.2 | ) | |||||

| Finance income | 15.4 | 4.2 | |||||||

| Finance expense | (19.0 | ) | (35.2 | ) | |||||

| Earnings before tax | 1,321.2 | 526.2 | |||||||

| Income tax expense | (465.2 | ) | (136.8 | ) | |||||

| Net earnings | $ | 856.0 | $ | 389.4 | |||||

| Net earnings attributable to: | |||||||||

| Non-controlling interests | $ | 13.0 | $ | 21.4 | |||||

| Common shareholders | $ | 843.0 | $ | 368.0 | |||||

| Earnings per share attributable to common shareholders | |||||||||

| Basic | $ | 0.70 | $ | 0.30 | |||||

| Diluted | $ | 0.70 | $ | 0.30 | |||||

Consolidated statements of cash flows

| (expressed in millions of U.S. dollars) | |||||||||

| Three months ended | |||||||||

| March 31, | March 31, | ||||||||

| 2026 | 2025 | ||||||||

| Net inflow (outflow) of cash related to the following activities: | |||||||||

| Operating: | |||||||||

| Net earnings | $ | 856.0 | $ | 389.4 | |||||

| Adjustments to reconcile net earnings to net cash provided from operating activities: | |||||||||

| Depreciation, depletion and amortization | 275.7 | 288.4 | |||||||

| Share-based compensation expense | 6.6 | 4.6 | |||||||

| Finance expense - net | 3.6 | 31.0 | |||||||

| Income tax expense | 465.2 | 136.8 | |||||||

| Foreign exchange losses | 7.5 | 5.5 | |||||||

| Other | (7.3 | ) | (21.0 | ) | |||||

| Reclamation payments, net of reclamation (recovery) expense | (10.1 | ) | (6.2 | ) | |||||

| Changes in working capital: | |||||||||

| Accounts receivable and other assets | 6.9 | 11.4 | |||||||

| Inventories | 35.8 | (38.4 | ) | ||||||

| Accounts payable and accrued liabilities | (51.8 | ) | (16.1 | ) | |||||

| Cash flow provided from operating activities | 1,588.1 | 785.4 | |||||||

| Income taxes paid | (448.6 | ) | (178.3 | ) | |||||

| Net cash flow provided from operating activities | 1,139.5 | 607.1 | |||||||

| Investing: | |||||||||

| Additions to property, plant and equipment | (283.2 | ) | (207.7 | ) | |||||

| Interest paid capitalized to property, plant and equipment | (7.1 | ) | (13.5 | ) | |||||

| Additions to long-term investments and other assets | (25.3 | ) | (9.1 | ) | |||||

| Increase in restricted cash - net | (1.8 | ) | (1.7 | ) | |||||

| Interest received and other - net | 15.1 | 4.2 | |||||||

| Net cash flow used in investing activities | (302.3 | ) | (227.8 | ) | |||||

| Financing: | |||||||||

| Repayment of debt | - | (200.0 | ) | ||||||

| Interest paid | (17.2 | ) | (24.0 | ) | |||||

| Payment of lease liabilities | (2.2 | ) | (1.5 | ) | |||||

| Distributions paid to non-controlling interest | (9.0 | ) | (24.0 | ) | |||||

| Dividends paid to common shareholders | (47.9 | ) | (36.9 | ) | |||||

| Payments for employee taxes withheld from restricted share unit releases | (55.3 | ) | (10.0 | ) | |||||

| Repurchase and cancellation of shares | (250.1 | ) | - | ||||||

| Taxes paid on repurchase of shares | (12.1 | ) | - | ||||||

| Net cash flow used in financing activities | (393.8 | ) | (296.4 | ) | |||||

| Effect of exchange rate changes on cash and cash equivalents | (0.7 | ) | 0.2 | ||||||

| Increase in cash and cash equivalents | 442.7 | 83.1 | |||||||

| Cash and cash equivalents, beginning of period | 1,742.3 | 611.5 | |||||||

| Cash and cash equivalents, end of period | $ | 2,185.0 | $ | 694.6 | |||||

| Operating Summary | |||||||||||||||||||

| Mine | Period | Tonnes Ore Mined | Ore Processed (Milled) | Ore Processed (Heap Leach) | Grade (Mill) | Grade (Heap Leach) | Recovery (a)(b) | Gold Eq Production(c) | Gold Eq Sales(c) | Production cost of sales | Production cost of sales/oz(d) | Cap Ex - sustaining(e) | Total Cap Ex (e) | ||||||

| ('000 tonnes) | ('000 tonnes) | ('000 tonnes) | (g/t) | (g/t) | (%) | (ounces) | (ounces) | ($ millions) | ($/ounce) | ($ millions) | ($ millions) | ||||||||

| West Africa | Tasiast | Q1 2026 | 3,495 | 2,092 | - | 2.30 | - | 94 | % | 130,014 | 131,679 | $ | 130.3 | $ | 990 | $ | 10.8 | $ | 60.0 |

| Q4 2025 | 3,120 | 2,252 | - | 1.87 | - | 94 | % | 125,625 | 118,912 | $ | 119.2 | $ | 1,002 | $ | 28.6 | $ | 80.5 | ||

| Q3 2025 | 1,685 | 2,181 | - | 1.78 | - | 94 | % | 120,934 | 116,251 | $ | 103.4 | $ | 889 | $ | 47.6 | $ | 102.0 | ||

| Q2 2025 | 1,921 | 1,730 | - | 2.11 | - | 95 | % | 119,241 | 121,745 | $ | 102.6 | $ | 843 | $ | 23.1 | $ | 89.7 | ||

| Q1 2025 | 1,812 | 1,932 | - | 2.15 | - | 95 | % | 137,629 | 129,493 | $ | 105.0 | $ | 811 | $ | 13.7 | $ | 80.1 | ||

| Americas | Paracatu | Q1 2026 | 10,272 | 12,507 | - | 0.41 | - | 85 | % | 160,583 | 158,849 | $ | 177.7 | $ | 1,119 | $ | 22.2 | $ | 25.8 |

| Q4 2025 | 10,929 | 12,395 | - | 0.45 | - | 83 | % | 155,048 | 154,565 | $ | 165.0 | $ | 1,068 | $ | 67.6 | $ | 67.6 | ||

| Q3 2025 | 12,958 | 13,214 | - | 0.44 | - | 82 | % | 150,367 | 149,903 | $ | 139.9 | $ | 933 | $ | 58.2 | $ | 58.2 | ||

| Q2 2025 | 13,497 | 14,527 | - | 0.39 | - | 82 | % | 149,264 | 148,787 | $ | 142.6 | $ | 958 | $ | 38.4 | $ | 38.4 | ||

| Q1 2025 | 13,318 | 12,507 | - | 0.43 | - | 83 | % | 146,639 | 146,855 | $ | 139.6 | $ | 951 | $ | 24.4 | $ | 24.4 | ||

| La Coipa(f) | Q1 2026 | 580 | 972 | - | 1.64 | - | 74 | % | 54,211 | 53,737 | $ | 82.0 | $ | 1,526 | $ | 19.9 | $ | 21.7 | |

| Q4 2025 | 1,219 | 1,203 | - | 2.42 | - | 74 | % | 67,319 | 71,419 | $ | 80.7 | $ | 1,130 | $ | 31.7 | $ | 31.7 | ||

| Q3 2025 | 1,006 | 932 | - | 2.36 | - | 76 | % | 57,997 | 57,544 | $ | 69.0 | $ | 1,199 | $ | 18.5 | $ | 18.5 | ||

| Q2 2025 | 580 | 911 | - | 1.77 | - | 78 | % | 54,139 | 50,400 | $ | 70.4 | $ | 1,397 | $ | 25.0 | $ | 25.0 | ||

| Q1 2025 | 1,265 | 971 | - | 2.19 | - | 80 | % | 52,315 | 55,870 | $ | 64.1 | $ | 1,147 | $ | 15.6 | $ | 15.6 | ||

| Fort Knox ( | Q1 2026 | 9,523 | 1,154 | 7,314 | 1.45 | 0.28 | 86 | % | 102,372 | 96,218 | $ | 174.8 | $ | 1,817 | $ | 24.1 | $ | 24.1 | |

| Q4 2025 | 11,056 | 1,645 | 8,805 | 1.02 | 0.23 | 88 | % | 71,523 | 74,294 | $ | 125.8 | $ | 1,693 | $ | 38.0 | $ | 38.0 | ||

| Q3 2025 | 8,140 | 1,511 | 6,538 | 1.86 | 0.23 | 90 | % | 112,181 | 117,500 | $ | 159.7 | $ | 1,359 | $ | 45.0 | $ | 45.0 | ||

| Q2 2025 | 7,639 | 1,636 | 5,529 | 1.72 | 0.23 | 88 | % | 115,064 | 113,200 | $ | 141.3 | $ | 1,248 | $ | 43.0 | $ | 43.0 | ||

| Q1 2025 | 6,530 | 1,071 | 4,790 | 2.77 | 0.19 | 91 | % | 112,054 | 112,110 | $ | 131.8 | $ | 1,176 | $ | 28.2 | $ | 28.2 | ||

| Fort Knox (attributable)(g) | Q1 2026 | 9,463 | 1,103 | 7,314 | 1.31 | 0.28 | 85 | % | 93,994 | 87,945 | $ | 154.9 | $ | 1,761 | $ | 19.8 | $ | 19.8 | |

| Q4 2025 | 11,001 | 1,597 | 8,805 | 0.93 | 0.23 | 87 | % | 65,434 | 67,882 | $ | 113.6 | $ | 1,673 | $ | 31.5 | $ | 31.5 | ||

| Q3 2025 | 8,056 | 1,425 | 6,538 | 1.55 | 0.23 | 89 | % | 95,742 | 100,878 | $ | 138.4 | $ | 1,372 | $ | 40.4 | $ | 40.4 | ||

| Q2 2025 | 7,535 | 1,567 | 5,529 | 1.47 | 0.23 | 87 | % | 97,561 | 95,277 | $ | 118.8 | $ | 1,247 | $ | 38.7 | $ | 38.7 | ||

| Q1 2025 | 6,445 | 982 | 4,790 | 2.35 | 0.19 | 90 | % | 94,281 | 94,585 | $ | 111.1 | $ | 1,175 | $ | 24.6 | $ | 24.6 | ||

| Round Mountain | Q1 2026 | 790 | 953 | 513 | 0.37 | 0.21 | 52 | % | 26,200 | 26,084 | $ | 72.4 | $ | 2,776 | $ | 4.9 | $ | 53.9 | |

| Q4 2025 | 737 | 966 | 1,110 | 0.49 | 0.29 | 67 | % | 31,754 | 31,641 | $ | 86.6 | $ | 2,737 | $ | 8.6 | $ | 41.5 | ||

| Q3 2025 | 1,659 | 914 | 1,113 | 0.66 | 0.32 | 72 | % | 37,297 | 37,274 | $ | 78.1 | $ | 2,095 | $ | 4.5 | $ | 33.0 | ||

| Q2 2025 | 2,881 | 856 | 1,682 | 0.72 | 0.30 | 80 | % | 38,665 | 37,864 | $ | 52.1 | $ | 1,376 | $ | 5.7 | $ | 32.8 | ||

| Q1 2025 | 1,927 | 856 | 2,163 | 0.66 | 0.27 | 77 | % | 35,686 | 35,960 | $ | 57.0 | $ | 1,585 | $ | 2.8 | $ | 29.6 | ||

| Bald Mountain | Q1 2026 | 3,985 | - | 3,985 | - | 0.30 | nm | 27,561 | 27,561 | $ | 53.3 | $ | 1,934 | $ | 6.9 | $ | 39.7 | ||

| Q4 2025 | 3,165 | - | 3,165 | - | 0.30 | nm | 38,402 | 37,141 | $ | 55.4 | $ | 1,492 | $ | 13.1 | $ | 51.6 | |||

| Q3 2025 | 2,182 | - | 2,182 | - | 0.31 | nm | 41,525 | 42,261 | $ | 48.5 | $ | 1,148 | $ | 5.3 | $ | 27.9 | |||

| Q2 2025 | 1,578 | - | 1,578 | - | 1.07 | nm | 53,704 | 54,227 | $ | 59.4 | $ | 1,095 | $ | 12.7 | $ | 40.4 | |||

| Q1 2025 | 5,803 | - | 5,803 | - | 0.35 | nm | 45,538 | 43,801 | $ | 49.2 | $ | 1,123 | $ | 6.9 | $ | 17.8 | |||

| (a) | Due to the nature of heap leach operations, recovery rates at Bald Mountain cannot be accurately measured on a quarterly basis. Recovery rates at Fort Knox and Round Mountain represent mill recovery only. |

| (b) | "nm" means not meaningful. |

| (c) | Gold equivalent ounces include silver ounces produced and sold converted to a gold equivalent based on the ratio of the average spot market prices for the commodities for each period. The ratios for the quarters presented are as follows: Q1 2026: 57.79:1; Q4 2025: 76.34:1; Q3 2025: 87.73:1; Q2 2025: 97.41:1; Q1 2025: 89.69:1. |

| (d) | “Production cost of sales per equivalent ounce sold” is defined as production cost of sales divided by total gold equivalent ounces sold. |

| (e) | "Total Cap Ex" is “Additions to property, plant and equipment” on the interim condensed consolidated statements of cash flows. "Cap Ex - sustaining" is a non-GAAP financial measure. The definition and reconciliation of this non-GAAP financial measure is included on pages 22 and 23 of this news release. |

| (f) | La Coipa silver grade and recovery were as follows: Q1 2026: 35.03 g/t, |

| (g) | The Fort Knox segment is composed of Fort Knox and Manh Choh. Manh Choh tonnes of ore processed and grade were as follows: Q1 2026: 170,077 tonnes, 4.51 g/t; Q4 2025: 158,016 tonnes, 4.08 g/t; Q3 2025: 286,496 tonnes, 7.05 g/t; Q2 2025: 231,451 tonnes, 7.39 g/t; Q1 2025: 294,238 tonnes, 7.39 g/t. The attributable results for Fort Knox include |

Reconciliation of non-GAAP financial measures and ratios

The Company has included certain non-GAAP financial measures and ratios in this document. These financial measures and ratios are not defined under IFRS and should not be considered in isolation. The Company believes that these financial measures and ratios, together with financial measures and ratios determined in accordance with IFRS, provide investors with an improved ability to evaluate the underlying performance of the Company. The inclusion of these financial measures and ratios is meant to provide additional information and should not be used as a substitute for performance measures prepared in accordance with IFRS. These financial measures and ratios are not necessarily standard and therefore may not be comparable to other issuers.

Adjusted Net Earnings and Adjusted Net Earnings per Share

Adjusted net earnings and adjusted net earnings per share are non-GAAP financial measures and ratios which determine the performance of the Company, excluding certain impacts which the Company believes are not reflective of the Company’s underlying performance for the reporting period, such as the impact of foreign exchange gains and losses, reassessment of prior year taxes and/or taxes otherwise not related to the current period, impairment charges (reversals), gains and losses and other one-time costs related to acquisitions, dispositions and other transactions, and non-hedge derivative gains and losses. Although some of the items are recurring, the Company believes that they are not reflective of the underlying operating performance of its current business and are not necessarily indicative of future operating results. Management believes that these measures and ratios, which are used internally to assess performance and in planning and forecasting future operating results, provide investors with the ability to better evaluate underlying performance, particularly since the excluded items are typically not included in public guidance. However, adjusted net earnings and adjusted net earnings per share measures and ratios are not necessarily indicative of net earnings and earnings per share measures and ratios as determined under IFRS.

The following table provides a reconciliation of net earnings to adjusted net earnings for the periods presented:

| (expressed in millions of U.S. dollars, except per share amounts) | Three months ended | ||||||

| March 31, | |||||||

| 2026 | 2025 | ||||||

| Net earnings attributable to common shareholders - as reported | $ | 843.0 | $ | 368.0 | |||

| Adjusting items: | |||||||

| Foreign exchange losses | 6.0 | 7.7 | |||||

| Foreign exchange gains on translation of tax basis and foreign exchange on deferred income taxes within income tax expense | (4.5 | ) | (5.9 | ) | |||

| Taxes in respect of prior periods | 2.2 | (7.9 | ) | ||||

| Costs in connection with conveyor belt repairs | 11.1 | - | |||||

| Other(a) | (1.6 | ) | 1.7 | ||||

| Tax effects of the above adjustments | (2.1 | ) | 0.4 | ||||

| 11.1 | (4.0 | ) | |||||

| Adjusted net earnings | $ | 854.1 | $ | 364.0 | |||

| Weighted average number of common shares outstanding - Basic | 1,199.5 | 1,229.6 | |||||

| Adjusted net earnings per share | $ | 0.71 | $ | 0.30 | |||

| Basic earnings per share attributable to common shareholders - as reported | $ | 0.70 | $ | 0.30 | |||

| (a) | Other includes various impacts, such as one-time costs and credits at sites, and gains and losses on hedges, which the Company believes are not reflective of the Company’s underlying performance for the reporting period. |

Attributable Free Cash Flow

Attributable free cash flow is a non-GAAP financial measure and is defined as net cash flow provided from operating activities less attributable capital expenditures and non-controlling interest included in net cash flows provided from operating activities. The Company believes that this measure, which is used internally to evaluate the Company’s underlying cash generation performance and the ability to repay creditors and return cash to shareholders, provides investors with the ability to better evaluate the Company’s underlying performance. However, this measure is not necessarily indicative of operating earnings or net cash flow provided from operating activities as determined under IFRS.

The following table provides a reconciliation of attributable free cash flow for the periods presented:

| (expressed in millions of U.S. dollars) | Three months ended | ||||||

| March 31, | |||||||

| 2026 | 2025 | ||||||

| Net cash flow provided from operating activities - as reported | $ | 1,139.5 | $ | 607.1 | |||

| Adjusting items: | |||||||

| Attributable(a) capital expenditures | (278.9 | ) | (204.1 | ) | |||

| Non-controlling interest(b) cash flow from operating activities | (23.1 | ) | (22.2 | ) | |||

| Attributable(a) free cash flow | $ | 837.5 | $ | 380.8 | |||

See pages 23 and 24 for details of the footnotes referenced within the table above.

Attributable Adjusted Operating Cash Flow

Attributable adjusted operating cash flow is a non-GAAP financial measure and is defined as net cash flow provided from operating activities excluding changes in working capital, certain impacts which the Company believes are not reflective of the Company’s regular operating cash flow, and net cash flows provided from operating activities, net of working capital changes, relating to non-controlling interests. Working capital is excluded given that numerous factors can result in it being volatile. The Company uses attributable adjusted operating cash flow internally as a measure of the underlying operating cash flow performance and future operating cash flow-generating capability of the Company. However, the attributable adjusted operating cash flow measure is not necessarily indicative of net cash flow provided from operating activities as determined under IFRS.

The following table provides a reconciliation of attributable adjusted operating cash flow for the periods presented:

| (expressed in millions of U.S. dollars) | Three months ended | ||||||

| March 31, | |||||||

| 2026 | 2025(m) | ||||||

| Net cash flow provided from operating activities - as reported | $ | 1,139.5 | $ | 607.1 | |||

| Adjusting items: | |||||||

| Working capital changes: | |||||||

| Accounts receivable and other assets | (6.9 | ) | (11.4 | ) | |||

| Inventories | (35.8 | ) | 38.4 | ||||

| Accounts payable and accrued liabilities | 51.8 | 16.1 | |||||

| 1,148.6 | 650.2 | ||||||

| Non-controlling interest(b) cash flow from operating activities, net of working capital changes | (19.3 | ) | (29.9 | ) | |||

| Attributable(a) adjusted operating cash flow | $ | 1,129.3 | $ | 620.3 | |||

See pages 23 and 24 for details of the footnotes referenced within the table above.

Attributable Average Realized Gold Price per Ounce

Attributable average realized gold price per ounce is a non-GAAP ratio which calculates the average price realized from gold sales attributable to the Company. The Company believes that this measure provides a more accurate measure with which to compare the Company's gold sales performance to market gold prices. The following table provides a reconciliation of attributable average realized gold price per ounce for the periods presented:

| (expressed in millions of U.S. dollars, except ounces and average realized gold price per ounce) | Three months ended | ||||||

| March 31, | |||||||

| 2026 | 2025 | ||||||

| Metal sales - as reported | $ | 2,407.7 | $ | 1,497.5 | |||

| Less: silver revenue(c) | (56.7 | ) | (22.5 | ) | |||

| Less: non-controlling interest(b) gold revenue | (38.9 | ) | (50.1 | ) | |||

| Attributable(a) gold revenue | $ | 2,312.1 | $ | 1,424.9 | |||

| Gold ounces sold | 482,472 | 516,268 | |||||

| Less: non-controlling interest(b) gold ounces sold | (8,013 | ) | (17,383 | ) | |||

| Attributable(a) gold ounces sold | 474,459 | 498,885 | |||||

| Attributable(a) average realized gold price per ounce | $ | 4,873 | $ | 2,856 | |||

| Average realized gold price per ounce(d) | $ | 4,873 | $ | 2,857 | |||

See pages 23 and 24 for details of the footnotes referenced within the table above.

Attributable Production Cost of Sales per Equivalent Ounce Sold

Production cost of sales per equivalent ounce sold is defined as production cost of sales, as reported on the consolidated statement of operations, divided by the total number of gold equivalent ounces sold. This measure converts the Company’s non-gold production into gold equivalent ounces and credits it to total production.

Attributable production cost of sales per equivalent ounce sold is a non-GAAP ratio and is defined as attributable production cost of sales divided by the attributable number of gold equivalent ounces sold. This measure converts the Company’s attributable non-gold production into gold equivalent ounces and credits it to total attributable production. Management uses this measure to monitor and evaluate the performance of its operating properties that are attributable to its shareholders.

The following table provides a reconciliation of production cost of sales and attributable production cost of sales per equivalent ounce sold for the periods presented:

| (expressed in millions of U.S. dollars, except ounces and production cost of sales per equivalent ounce) | Three months ended | ||||||

| March 31, | |||||||

| 2026 | 2025 | ||||||

| Production cost of sales - as reported | $ | 690.5 | $ | 546.7 | |||

| Less: non-controlling interest(b) production cost of sales | (19.9 | ) | (20.7 | ) | |||

| Attributable(a) production cost of sales | $ | 670.6 | $ | 526.0 | |||

| Gold equivalent ounces sold | 494,128 | 524,089 | |||||

| Less: non-controlling interest(b) gold equivalent ounces sold | (8,273 | ) | (17,525 | ) | |||

| Attributable(a) gold equivalent ounces sold | 485,855 | 506,564 | |||||

| Attributable(a) production cost of sales per equivalent ounce sold | $ | 1,380 | $ | 1,038 | |||

| Production cost of sales per equivalent ounce sold(e) | $ | 1,397 | $ | 1,043 | |||

See pages 23 and 24 for details of the footnotes referenced within the table above.

Attributable Production Cost of Sales per Ounce Sold on a By-Product Basis

Attributable production cost of sales per ounce sold on a by-product basis is a non-GAAP ratio which calculates the Company’s non-gold production as a credit against its per ounce production costs, rather than converting its non-gold production into gold equivalent ounces and crediting it to total production, as is the case in co-product accounting. Management believes that this ratio provides investors with the ability to better evaluate Kinross’ production cost of sales per ounce on a comparable basis with other major gold producers who routinely calculate their cost of sales per ounce using by-product accounting rather than co-product accounting.

The following table provides a reconciliation of attributable production cost of sales per ounce sold on a by-product basis for the periods presented:

| (expressed in millions of U.S. dollars, except ounces and production cost of sales per ounce) | Three months ended | ||||||

| March 31, | |||||||

| 2026 | 2025 | ||||||

| Production cost of sales - as reported | $ | 690.5 | $ | 546.7 | |||

| Less: non-controlling interest(b) production cost of sales | (19.9 | ) | (20.7 | ) | |||

| Less: attributable(a) impact of silver by-product(n) | (55.5 | ) | (22.1 | ) | |||

| Attributable(a) production cost of sales on a by-product basis | $ | 615.1 | $ | 503.9 | |||

| Gold ounces sold | 482,472 | 516,268 | |||||

| Less: non-controlling interest(b) gold ounces sold | (8,013 | ) | (17,383 | ) | |||

| Attributable(a) gold ounces sold | 474,459 | 498,885 | |||||

| Attributable(a) production cost of sales per ounce sold on a by-product basis | $ | 1,296 | $ | 1,010 | |||

| Production cost of sales per equivalent ounce sold(e) | $ | 1,397 | $ | 1,043 | |||

See pages 23 and 24 for details of the footnotes referenced within the table above.

Attributable All-In Sustaining Cost and All-In Cost per Ounce Sold on a By-Product Basis

Attributable all-in sustaining cost and all-in cost per ounce sold on a by-product basis are non-GAAP financial measures and ratios, as applicable, calculated based on guidance published by the World Gold Council (“WGC”). The WGC is a market development organization for the gold industry and is an association whose membership comprises leading gold mining companies including Kinross. Although the WGC is not a mining industry regulatory organization, it worked closely with its member companies to develop these metrics. Adoption of the all-in sustaining cost and all-in cost metrics is voluntary and not necessarily standard, and therefore, these measures and ratios presented by the Company may not be comparable to similar measures and ratios presented by other issuers. The Company believes that the all-in sustaining cost and all-in cost measures complement existing measures and ratios reported by Kinross.

All-in sustaining cost includes both operating and capital costs required to sustain gold production on an ongoing basis. The value of silver sold is deducted from the total production cost of sales as it is considered residual production, i.e. a by-product. Sustaining operating costs represent expenditures incurred at current operations that are considered necessary to maintain current production. Sustaining capital represents capital expenditures at existing operations comprising mine development costs, including capitalized development, and ongoing replacement of mine equipment and other capital facilities, and does not include capital expenditures for major growth projects or enhancement capital for significant infrastructure improvements at existing operations.

All-in cost is comprised of all-in sustaining cost as well as operating expenditures incurred at locations with no current operation, or costs related to other non-sustaining activities, and capital expenditures for major growth projects or enhancement capital for significant infrastructure improvements at existing operations.

Attributable all-in sustaining cost and all-in cost per ounce sold on a by-product basis are calculated by adjusting production cost of sales, as reported on the consolidated statements of operations, as follows:

| (expressed in millions of U.S. dollars, except ounces and costs per ounce) | Three months ended | ||||||

| March 31, | |||||||

| 2026 | 2025 | ||||||

| Production cost of sales - as reported | $ | 690.5 | $ | 546.7 | |||

| Less: non-controlling interest(b) production cost of sales | (19.9 | ) | (20.7 | ) | |||

| Less: attributable(a) impact of silver by-product(n) | (55.5 | ) | (22.1 | ) | |||

| Attributable(a) production cost of sales on a by-product basis | $ | 615.1 | $ | 503.9 | |||

| Adjusting items on an attributable(a) basis: | |||||||

| General and administrative(f) | 44.9 | 35.7 | |||||

| Other operating expense - sustaining(g) | 0.2 | 0.2 | |||||

| Reclamation and remediation - sustaining(h) | 23.1 | 22.3 | |||||

| Exploration and business development - sustaining(i) | 16.1 | 12.5 | |||||

| Additions to property, plant and equipment - sustaining(j) | 84.6 | 88.2 | |||||

| Lease payments - sustaining(k) | 2.0 | 1.3 | |||||

| All-in Sustaining Cost on a by-product basis - attributable(a) | $ | 786.0 | $ | 664.1 | |||

| Adjusting items on an attributable(a) basis: | |||||||

| Other operating expense - non-sustaining(g) | 8.5 | 16.2 | |||||

| Reclamation and remediation - non-sustaining(h) | 2.1 | 2.3 | |||||

| Exploration and business development - non-sustaining(i) | 21.7 | 29.4 | |||||

| Additions to property, plant and equipment - non-sustaining(j) | 194.3 | 115.9 | |||||

| Lease payments - non-sustaining(k) | 0.2 | 0.2 | |||||

| All-in Cost on a by-product basis - attributable(a) | $ | 1,012.8 | $ | 828.1 | |||

| Gold ounces sold | 482,472 | 516,268 | |||||

| Less: non-controlling interest(b) gold ounces sold | (8,013 | ) | (17,383 | ) | |||

| Attributable(a) gold ounces sold | 474,459 | 498,885 | |||||

| Attributable(a) all-in sustaining cost per ounce sold on a by-product basis | $ | 1,657 | $ | 1,331 | |||

| Attributable(a) all-in cost per ounce sold on a by-product basis | $ | 2,135 | $ | 1,660 | |||

| Production cost of sales per equivalent ounce sold(e) | $ | 1,397 | $ | 1,043 | |||

See pages 23 and 24 for details of the footnotes referenced within the table above.

Attributable All-In Sustaining Cost and All-In Cost per Equivalent Ounce Sold

The Company also assesses its attributable all-in sustaining cost and all-in cost on a gold equivalent ounce basis. Under these non-GAAP financial measures and ratios, the Company’s production of silver is converted into gold equivalent ounces and credited to total production.

Attributable all-in sustaining cost and all-in cost per equivalent ounce sold are calculated by adjusting production cost of sales, as reported on the consolidated statements of operations, as follows:

| (expressed in millions of U.S. dollars, except ounces and costs per ounce) | Three months ended | ||||||

| March 31, | |||||||

| 2026 | 2025 | ||||||

| Production cost of sales - as reported | $ | 690.5 | $ | 546.7 | |||

| Less: non-controlling interest(b) production cost of sales | (19.9 | ) | (20.7 | ) | |||

| Attributable(a) production cost of sales | $ | 670.6 | $ | 526.0 | |||

| Adjusting items on an attributable(a) basis: | |||||||

| General and administrative(f) | 44.9 | 35.7 | |||||

| Other operating expense - sustaining(g) | 0.2 | 0.2 | |||||

| Reclamation and remediation - sustaining(h) | 23.1 | 22.3 | |||||

| Exploration and business development - sustaining(i) | 16.1 | 12.5 | |||||

| Additions to property, plant and equipment - sustaining(j) | 84.6 | 88.2 | |||||

| Lease payments - sustaining(k) | 2.0 | 1.3 | |||||

| All-in Sustaining Cost - attributable(a) | $ | 841.5 | $ | 686.2 | |||

| Adjusting items on an attributable(a) basis: | |||||||

| Other operating expense - non-sustaining(g) | 8.5 | 16.2 | |||||

| Reclamation and remediation - non-sustaining(h) | 2.1 | 2.3 | |||||

| Exploration and business development - non-sustaining(i) | 21.7 | 29.4 | |||||

| Additions to property, plant and equipment - non-sustaining(j) | 194.3 | 115.9 | |||||

| Lease payments - non-sustaining(k) | 0.2 | 0.2 | |||||

| All-in Cost - attributable(a) | $ | 1,068.3 | $ | 850.2 | |||

| Gold equivalent ounces sold | 494,128 | 524,089 | |||||

| Less: non-controlling interest(b) gold equivalent ounces sold | (8,273 | ) | (17,525 | ) | |||

| Attributable(a) gold equivalent ounces sold | 485,855 | 506,564 | |||||

| Attributable(a) all-in sustaining cost per equivalent ounce sold | $ | 1,732 | $ | 1,355 | |||

| Attributable(a) all-in cost per equivalent ounce sold | $ | 2,199 | $ | 1,678 | |||

| Production cost of sales per equivalent ounce sold(e) | $ | 1,397 | $ | 1,043 | |||

See pages 23 and 24 for details of the footnotes referenced within the table above.

Capital Expenditures and Attributable Capital Expenditures

Capital expenditures are classified as either sustaining capital expenditures or non-sustaining capital expenditures, depending on the nature of the expenditure. Sustaining capital expenditures typically represent capital expenditures at existing operations including capitalized exploration costs and capitalized development unless related to major projects, ongoing replacement of mine equipment and other capital facilities and other capital expenditures and is calculated as total additions to property, plant and equipment (as reported on the consolidated statements of cash flows), less non-sustaining capital expenditures. Non-sustaining capital expenditures represent capital expenditures for major projects, including major capital development projects at existing operations that are expected to materially benefit the operation, as well as enhancement capital for significant infrastructure improvements at existing operations. Management believes the distinction between sustaining capital expenditures and non-sustaining expenditures is a useful indicator of the purpose of capital expenditures and this distinction is an input into the calculation of attributable all-in sustaining costs per ounce and attributable all-in costs per ounce. The categorization of sustaining capital expenditures and non-sustaining capital expenditures is consistent with the definitions under the WGC all-in cost standard. Sustaining capital expenditures and non-sustaining capital expenditures are not defined under IFRS, however, the sum of these two measures total to additions to property, plant and equipment as disclosed under IFRS on the consolidated statements of cash flows.

Additions to property, plant and equipment per the consolidated statements of cash flows includes

The following table provides a reconciliation of the classification of capital expenditures for the periods presented:

| (expressed in millions of U.S. dollars) | |||||||||||||||||||||

| Three months ended March 31, 2026 | Tasiast (Mauritania) | Paracatu (Brazil) | La Coipa (Chile) | Fort Knox(l)(USA) | Round Mountain (USA) | Bald Mountain (USA) | Total USA | Other | Total | ||||||||||||

| Sustaining capital expenditures | $ | 10.8 | $ | 22.2 | $ | 19.9 | $ | 24.1 | $ | 4.9 | $ | 6.9 | $ | 35.9 | $ | 0.1 | $ | 88.9 | |||

| Non-sustaining capital expenditures | 49.2 | 3.6 | 1.8 | - | 49.0 | 32.8 | 81.8 | 57.9 | 194.3 | ||||||||||||

| Additions to property, plant and equipment - per cash flow | $ | 60.0 | $ | 25.8 | $ | 21.7 | $ | 24.1 | $ | 53.9 | $ | 39.7 | $ | 117.7 | $ | 58.0 | $ | 283.2 | |||

| Less: Non-controlling interest(b) | $ | - | $ | - | $ | - | $ | (4.3 | ) | $ | - | $ | - | $ | (4.3 | ) | $ | - | $ | (4.3 | ) |

| Attributable(a) capital expenditures | $ | 60.0 | $ | 25.8 | $ | 21.7 | $ | 19.8 | $ | 53.9 | $ | 39.7 | $ | 113.4 | $ | 58.0 | $ | 278.9 | |||

| Three months ended March 31, 2025 | |||||||||||||||||||||

| Sustaining capital expenditures | $ | 13.7 | $ | 24.4 | $ | 15.6 | $ | 28.2 | $ | 2.8 | $ | 6.9 | $ | 37.9 | $ | 0.2 | $ | 91.8 | |||

| Non-sustaining capital expenditures | 66.4 | - | - | - | 26.8 | 10.9 | 37.7 | 11.8 | 115.9 | ||||||||||||

| Additions to property, plant and equipment - per cash flow | $ | 80.1 | $ | 24.4 | $ | 15.6 | $ | 28.2 | $ | 29.6 | $ | 17.8 | $ | 75.6 | $ | 12.0 | $ | 207.7 | |||

| Less: Non-controlling interest(b) | $ | - | $ | - | $ | - | $ | (3.6 | ) | $ | - | $ | - | $ | (3.6 | ) | $ | - | $ | (3.6 | ) |

| Attributable(a)capital expenditures | $ | 80.1 | $ | 24.4 | $ | 15.6 | $ | 24.6 | $ | 29.6 | $ | 17.8 | $ | 72.0 | $ | 12.0 | $ | 204.1 | |||

See pages 23 and 24 for details of the footnotes referenced within the tables above.

Endnotes

| (a) | “Attributable” measures and ratios include Kinross’ share of Manh Choh ( |

| (b) | “Non-controlling interest” represents the non-controlling interest portion in Manh Choh ( |

| (c) | “Silver revenue” represents the portion of metal sales realized from the production of secondary or by-product metal (i.e. silver), which is produced as a by-product of the process used to produce gold and effectively reduces the cost of gold production. |

| (d) | “Average realized gold price per ounce” is defined as gold revenue divided by total gold ounces sold. |

| (e) | “Production cost of sales per equivalent ounce sold” is defined as production cost of sales divided by total gold equivalent ounces sold. |

| (f) | “General and administrative” expenses are as reported on the consolidated statements of operations, excluding certain impacts which the Company believes are not reflective of the Company’s underlying performance for the reporting period. General and administrative expenses are considered sustaining costs as they are required to be absorbed on a continuing basis for the effective operation and governance of the Company. |

| (g) | “Other operating expense – sustaining” is calculated as “Other operating expense” as reported on the consolidated statements of operations, less the non-controlling interest portion in Manh Choh ( |

| (h) | “Reclamation and remediation – sustaining” is calculated as current period accretion related to reclamation and remediation obligations plus current period amortization of the corresponding reclamation and remediation assets, less the non-controlling interest portion in Manh Choh ( |

| (i) | “Exploration and business development – sustaining” is calculated as “Exploration and business development” expenses as reported on the consolidated statements of operations, less the non-controlling interest portion in Manh Choh ( |

| (j) | “Additions to property, plant and equipment – sustaining” and “non-sustaining” are as presented on pages 22 and 23 of this news release and include Kinross’ share of Manh Choh’s ( |

| (k) | “Lease payments – sustaining” represents the majority of lease payments as reported on the consolidated statements of cash flows and is made up of the principal and financing components of such cash payments, less the non-controlling interest portion in Manh Choh ( |

| (l) | The Fort Knox segment is composed of Fort Knox and Manh Choh for all periods presented. |

| (m) | Attributable adjusted operating cash flow for the three months ended March 31, 2025 has been presented in accordance with the current period’s presentation. |

| (n) | “Impact of silver by-product” represents the costs allocated to the production of secondary or by-product metal (i.e. silver), which is produced as a by-product of the process used to produce gold. |

Cautionary statement on forward-looking information

All statements, other than statements of historical fact, contained or incorporated by reference in this news release including, but not limited to, any information as to the future financial or operating performance of Kinross, constitute “forward-looking information” or “forward-looking statements” within the meaning of certain securities laws, including the provisions of the Securities Act (Ontario) and the provisions for “safe harbor” under the United States Private Securities Litigation Reform Act of 1995 and are based on expectations, estimates and projections as of the date of this news release. Forward-looking statements contained in this news release, include, but are not limited to, those under the headings (or headings that include) “2026 first-quarter highlights”, “Return of capital to shareholders”, “CEO commentary”, “Outlook”, and “Development projects”, as well as statements with respect to our guidance for production, cost guidance, including production costs of sales, all-in sustaining cost of sales, and capital expenditures; anticipated returns of capital to shareholders, including the declaration, payment, increase and sustainability of the Company’s dividends; the size, scope and execution of the proposed share buybacks and the anticipated timing thereof, including the Company’s statement targeting dividends and share buybacks for 2026 of

Key Sensitivities

Approximately

A

Specific to the Brazilian real, a

Specific to the Chilean peso, a

A

A

Other information

Where we say "we", "us", "our", the "Company", or "Kinross" in this news release, we mean Kinross Gold Corporation and/or one or more or all of its subsidiaries, as may be applicable.

The technical information about the Company’s mineral properties contained in this news release has been prepared under the supervision of Mr. Nicos Pfeiffer, an officer of the Company who is a “qualified person” within the meaning of National Instrument 43-101.

Source: Kinross Gold Corporation

________________________

1 Unless otherwise stated, production figures in this news release are on an attributable basis. “Attributable” includes Kinross’

2 “Production cost of sales per equivalent ounce sold” is defined as production cost of sales, as reported on the interim condensed consolidated statements of operations, divided by total gold equivalent ounces sold.

3 Operating cash flow figures in this release represent “Net cash flow provided from operating activities,” as reported on the interim condensed consolidated statements of cash flows.

4 “Margins” per equivalent ounce sold is defined as average realized gold price per ounce less production cost of sales per equivalent ounce sold.

5 Earnings, net earnings, and reported net earnings figures in this news release represent “Net earnings attributable to common shareholders,” as reported on the interim condensed consolidated statements of operations.

6 These figures are non-GAAP financial measures and ratios, as applicable, and are defined and reconciled on pages 17 to 23 of this news release. Non-GAAP financial measures and ratios have no standardized meaning under International Financial Reporting Standards (“IFRS”) and therefore, may not be comparable to similar measures presented by other issuers.

7 “Total liquidity” is defined as the sum of cash and cash equivalents, as reported on the interim condensed consolidated balance sheets, and available credit under the Company’s credit facilities (as calculated in Section 6 Liquidity and Capital Resources of Kinross’ MD&A for the three months ended March 31, 2026).

8 “Average realized gold price per ounce” is defined as gold revenue divided by total gold ounces sold.

9 “Capital expenditures” is “Additions to property, plant and equipment” on the interim condensed consolidated statements of cash flows.

10 “Available credit” is defined as available credit under the Company’s credit facilities and is calculated in Section 6 Liquidity and Capital Resources of Kinross’ MD&A for the three months ended March 31, 2026.

11 Based on

12 Taking into account existing oil hedges.

13 “AISC” represents attributable all-in sustaining cost per equivalent ounce sold. Refer to footnote 1.

14 Refer to 2021 press release “Kinross issues results of Udinsk and Lobo-Marte project studies”.

15 Refers to all of the currencies in the countries where the Company has mining operations, fluctuating simultaneously by