Commencement Bancorp, Inc. (CBWA) Announces Second Quarter 2025 Results

Rhea-AI Summary

Commencement Bancorp (OTCQX:CBWA) reported strong financial results for Q2 2025, with net income of $1.5 million ($0.40 per share), up from $1.3 million in Q1 2025 and $776,000 in Q2 2024. The bank demonstrated robust growth with loans receivable increasing by $37.9 million (32.4% annualized) and deposits growing by $20.5 million (14.4% annualized).

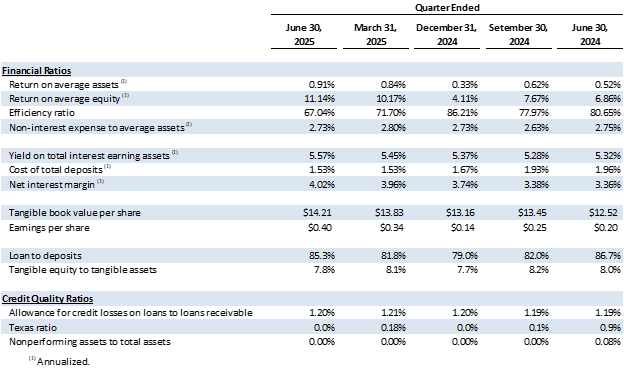

Key performance metrics showed improvement with net interest margin expanding to 4.02% from 3.96% in Q1 2025. The bank maintained strong credit quality with zero nonperforming assets and an allowance for credit losses at 1.20%. Total assets reached $681.7 million, supported by ample liquidity of $133.5 million and strong capital ratios above regulatory requirements.

Positive

- Net income increased 93.3% year-over-year to $1.5 million

- Strong loan growth of 32.4% annualized with $62.3M in new loan commitments

- Net interest margin improved to 4.02%, up 66 basis points year-over-year

- Zero nonperforming assets and improved classified loans ratio to 1.69%

- Robust liquidity position at 19.6% of total assets

Negative

- Required $15 million FHLB borrowing at 4.50% to fund loan growth

- Non-interest expenses increased 2.3% quarter-over-quarter

- Unrealized losses in investment securities increased by $88,000

News Market Reaction – CBWA

In the trading session that priced this news, CBWA gained 0.66%, reflecting a mild positive market reaction.

Data tracked by StockTitan Argus on the day of publication.

AI-generated analysis. How Rhea-AI works. Not financial advice.

2025 Second Quarter Financial Highlights:

Net income was

$1.5 million compared to$1.3 million for the first quarter of 2025 and$776,000 for the second quarter of 2024.Loans receivable increased

$37.9 million , or32.4% annualized growth rate.Deposits increased

$20.5 million , or14.4% annualized growth rate.Net interest margin increased to

4.02% from3.96% during the first quarter of 2025.Total cost of deposits remained steady at

1.53% .The Bank had no nonperforming assets as of June 30, 2025.

Capital ratios remained well above regulatory requirements.

TACOMA, WA / ACCESS Newswire / July 29, 2025 / Commencement Bancorp, Inc. (OTCQX:CBWA) (the "Company", "we," or "us"), the parent company of Commencement Bank (the "Bank") reported net income of

"We are pleased with our continued net interest margin expansion in 2025, resulting in an improvement of 58 basis points over the same period in 2024. Due to the hard work of our bankers, we are reaping the rewards of higher loan volumes and increased yields, which when combined with our focus on managing our overall cost of funds, has resulted in improved profitability. Our capital and liquidity remain strong, and our reputation as the trusted local bank is allowing us to exceed our loan growth goals for the year," said John E. Manolides, Chief Executive Officer.

"Our bankers' calling activity and business development throughout the past several months has started to materialize, which was evidenced in the second quarter. I'm proud of their resilience while competing, building trust, and earning new lending, deposit, and treasury relationships. Our heightened brand and style of banking continues to resonate in the markets we serve, and it's rewarding to see our strong performance during the quarter," said Nigel L. English, President & Chief Operating Officer.

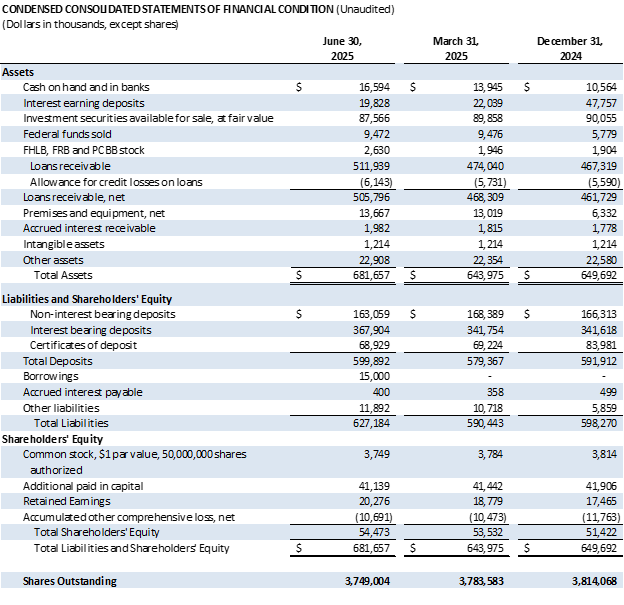

Balance Sheet

Total assets increased to

Investment securities available for sale decreased

Loans receivable increased

Total deposits increased

Total borrowings were

Credit Quality

The Bank had no nonperforming assets at June 30, 2025 or March 31, 2025. The allowance for credit losses to loan receivable remains strong at

The percentage of classified loans (loans rated Substandard or worse) to loans receivable improved to

Liquidity

The Bank has ample liquidity with both on- and off-balance sheet sources. Total on-balance sheet liquidity of

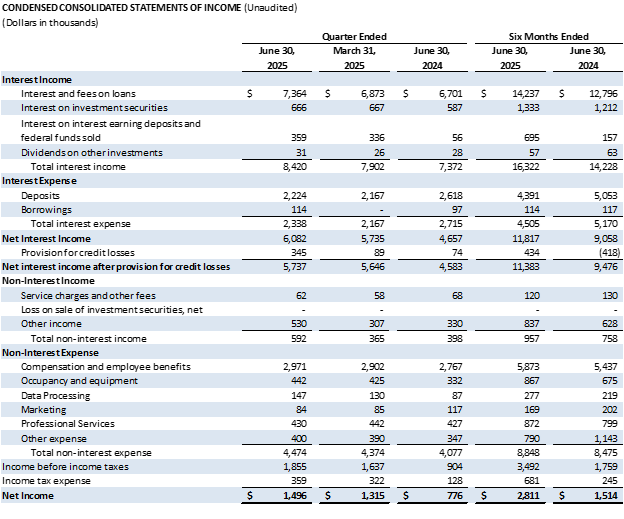

Income Statement

Net interest income increased

Interest income on loans increased

Interest expense on deposits increased

Interest expense on borrowings increased to

Total non-interest income increased

Total non-interest expense increased

###

About Commencement Bancorp, Inc.

Commencement Bancorp, Inc. is the holding company for Commencement Bank, headquartered in Tacoma, Washington. Commencement Bank was formed in 2006 to provide traditional, reliable, and sustainable banking in Pierce, King, and Thurston counties and the surrounding areas. Their team of experienced banking experts focuses on personal attention, flexible service, and building strong relationships with customers through state-of-the-art technology as well as traditional delivery systems. As a local bank, Commencement Bank is deeply committed to the community. For more information, please visit www.commencementbank.com. For information related to the trading of CBWA, please visit www.otcmarkets.com.

For further discussion, please contact the following:

John E. Manolides,Chief Executive Officer | 253-284-1802

Nigel L. English, President & Chief Operating Officer | 253-284-1801

Brandi Parker, Executive Vice President & Chief Financial Officer | 253-284-1803

Forward-Looking Statement Safe Harbor: This news release contains comments or information that constitutes forward-looking statements (within the meaning of the Private Securities Litigation Reform Act of 1995) that are based on current expectations that involve a number of risks and uncertainties. Forward-looking statements describe Commencement Bancorp, Inc.'s projections, estimates, plans and expectations of future results and can be identified by words such as "believe," "intend," "estimate," "likely," "anticipate," "expect," "looking forward," and other similar expressions. They are not guarantees of future performance. Actual results may differ materially from the results expressed in these forward-looking statements, which because of their forward-looking nature, are difficult to predict. Investors should not place undue reliance on any forward-looking statement, and should consider factors that might cause differences including but not limited to the degree of competition by traditional and nontraditional competitors, declines in real estate markets, an increase in unemployment or sustained high levels of unemployment; changes in interest rates; greater than expected costs to integrate acquisitions, adverse changes in local, national and international economies; changes in the Federal Reserve's actions that affect monetary and fiscal policies; changes in legislative or regulatory actions or reform, including without limitation, the Dodd-Frank Wall Street Reform and Consumer Protection Act; demand for products and services; changes to the quality of the loan portfolio and our ability to succeed in our problem-asset resolution efforts; the impact of technological advances; changes in tax laws; and other risk factors. Commencement Bancorp, Inc.undertakes no obligation to publicly update or clarify any forward-looking statement to reflect the impact of events or circumstances that may arise after the date of this release.

SOURCE: Commencement Bank

View the original press release on ACCESS Newswire