PULSE® Study Finds Debit’s Importance to Consumers Continues to Increase

Card-Not-Present Transactions Account for

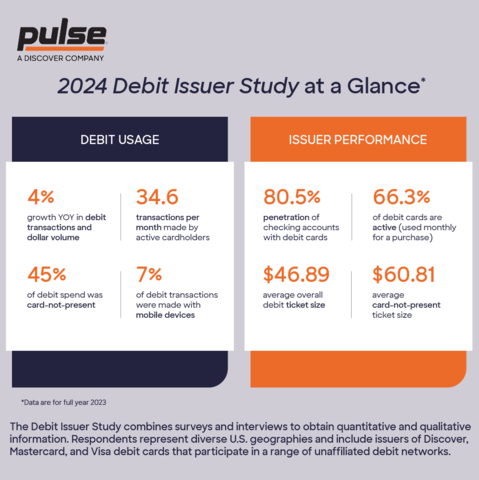

The 2024 PULSE Debit Issuer Study found more

“The ease and convenience of debit has made it a cornerstone of the retail banking customer experience,” said Steve Sievert, executive vice president of Marketing and Brand Management with PULSE. “With active cardholders now using debit for more than 400 transactions per year, a debit card serves as a daily reminder of the value of the relationship between a consumer and their financial institution.”

Debit Used Daily

The 2024 Debit Issuer Study found the number of debit transactions is growing faster than spend. Active cardholders completed 34.6 transactions per month in 2023, including 30.7 point-of-sale (POS) transactions, 2 account-to-account transfers, and 1.9 ATM transactions. POS use grew at an average annual rate of

Issuers reported a debit penetration rate (percentage of accounts with an associated debit card) of

Card-not-Present (CNP) Gained Share

Mobile and Digital Trends

Mobile devices originated

Issuers reported an average of three digital wallet transactions per active card per month in 2023, with an average value of

Digital issuance, through which an institution pushes debit card credentials directly to the digital wallet prior to physical card issuance, is the number one new capability issuers plan to introduce. Half of issuers reported plans to add digital instant-issuance capabilities. Benefits of digital issuance include superior convenience, no lag to use, and significant cost savings for the institution.

Debit Faces Shifting Dynamics

In addition to benefiting from debit’s continued growth and evolution, issuers are responding to three macro trends impacting debit:

-

A pending reduction in Regulation II’s interchange cap for covered issuers (those with

$10 billion - Increased competition from both traditional institutions and digital challengers.

- The potential impacts of real-time payments growth.

As issuers respond to these developments, they revealed three key priorities for the remainder of 2024 and into 2025:

- Continue to optimize penetration, active, and usage rates.

- Strengthen their fight against fraud.

- Invest in new digital capabilities, such as instant digital issuance and cardholder visibility into recurring payments.

For more information, visit the PULSE Debit Issuer Study resource center.

About the Study

The 2024 Debit Issuer Study is the 19th installment in the study series, commissioned by PULSE and conducted by Banking & Payments Group, an independent management consulting firm that specializes in the retail payments market. The study provides an objective fact base on debit issuer performance and financial institutions’ outlook for the debit business. Study respondents included large banks, credit unions and community banks. The sample is representative of the

About PULSE

PULSE is a leader in debit payments, global cash access, and account transfers, and we deliver exceptional value, choice, and convenience to clients across the payments ecosystem. We enable reliable and secure digital money movement for a wide variety of debit card programs through our PULSE Network, the Discover® Debit program, an advanced fraud-detection platform, and partner-support services. Our commitment to continuous improvement, innovation, and prioritizing the unique business needs of our clients empowers payment solutions that meet the evolving demands of consumers. PULSE is a Discover (NYSE: DFS) company and part of the Discover Global Network. For more information, visit PulseNetwork.com.

View source version on businesswire.com: https://www.businesswire.com/news/home/20240808048611/en/

Anne Uwabor, 832-214-0234

PULSE

anneuwabor@pulsenetwork.com

Dan Keeney, 800-596-8708

DPK Public Relations

dan@dpkpr.com

Source: PULSE