Ero Delivers Record Q4 Production and Strong Year-End Liquidity; Gold Concentrate Sales to Continue Through Mid-2027, Positioning for Next Phase of Step-Change Growth

Rhea-AI Summary

Ero (TSX/NYSE: ERO) reported record 2025 copper production of 64,307 tonnes and total gold of 52,290 ounces, with Q4 copper at 19,706 tonnes and Q4 gold at 13,837 ounces. Year-end liquidity was ~$150 million. 2026 guidance: consolidated copper 67,500–77,500 tonnes and copper C1 cash costs $2.15–$2.35/lb. Capital expenditures of $275–$320 million, including ~$80 million for Pilar shaft; Furnas PEA expected H1 2026. Gold concentrate sales from Xavantina to continue through mid-2027.

Positive

- Consolidated copper production 64,307 tonnes in 2025

- Year-end liquidity approximately $150 million

- 2026 consolidated copper guidance up to 20% higher

- Gold concentrate sales added 14,999 ounces in Q4 2025

- Pilar shaft capital of approximately $80 million underway

- Furnas PEA expected in H1 2026 after 50,000m drilling

Negative

- 2026 consolidated capital expenditures $275–$320 million

- Xavantina 2026 gold C1 cash cost $1,000–$1,250/oz

- Consolidated copper C1 cash cost guidance $2.15–$2.35/lb

News Market Reaction – ERO

In the Feb 5 session, ERO declined 10.47%, reflecting a significant negative market reaction. Argus tracked a trough of -13.7% from its starting point during tracking. Our momentum scanner triggered 21 alerts that day, indicating elevated trading interest and price volatility.

Data tracked by StockTitan Argus on the day of publication.

Key Figures

Historical Context

| Date | Event | Sentiment | 24h Move | Catalyst |

|---|---|---|---|---|

| Jan 30 | Results timing announcement | Neutral | +2.0% | Set dates for Q4 and full-year 2025 results and conference call. |

| Dec 19 | Technical report filing | Positive | +2.4% | Filed NI 43-101 technical report supporting updated Xavantina reserves/resources. |

| Nov 04 | Q3 2025 results | Positive | -3.5% | Reported record Q3 copper output, solid margins, and reaffirmed full-year guidance. |

| Nov 04 | Value-creation update | Positive | -3.5% | Announced Xavantina gold concentrate initiative and updated reserve/resource estimates. |

| Oct 07 | Earnings call scheduling | Neutral | +0.9% | Announced timing and access details for Q3 2025 results release and call. |

24h Move is the share-price change in the day after each event; other market factors may also have contributed.

Operationally positive updates, including production records and technical reports, have sometimes seen mixed market reactions, with both aligned gains and divergences where the stock fell on constructive news.

Over the last few months, Ero reported record Q3 2025 copper production of 16,664 tonnes at a blended C1 cash cost of $2.00/lb, solid liquidity of $111.3M, and initiated a value‑creation program at Xavantina with maiden inferred concentrate resources of ~29,000 oz. A subsequent technical report for Xavantina and scheduling announcements for Q3 and full‑year 2025 results reinforced an execution and disclosure cadence that this new record‑production and guidance update continues.

Key Terms

c1 cash cost financial

all-in sustaining costs financial

aisc financial

ni 43-101 regulatory

non-ifrs financial

ifrs financial

form s-8 regulatory

form f-10 regulatory

AI-generated analysis. How Rhea-AI works. Not financial advice.

(all amounts in US dollars, unless otherwise noted)

VANCOUVER, British Columbia, Feb. 05, 2026 (GLOBE NEWSWIRE) -- Ero Copper Corp. (TSX: ERO, NYSE: ERO) ("Ero" or the “Company”) is pleased to announce record 2025 copper production and provide 2026 guidance and an updated three-year production outlook.

HIGHLIGHTS

Fourth Quarter and Full Year 2025 Results

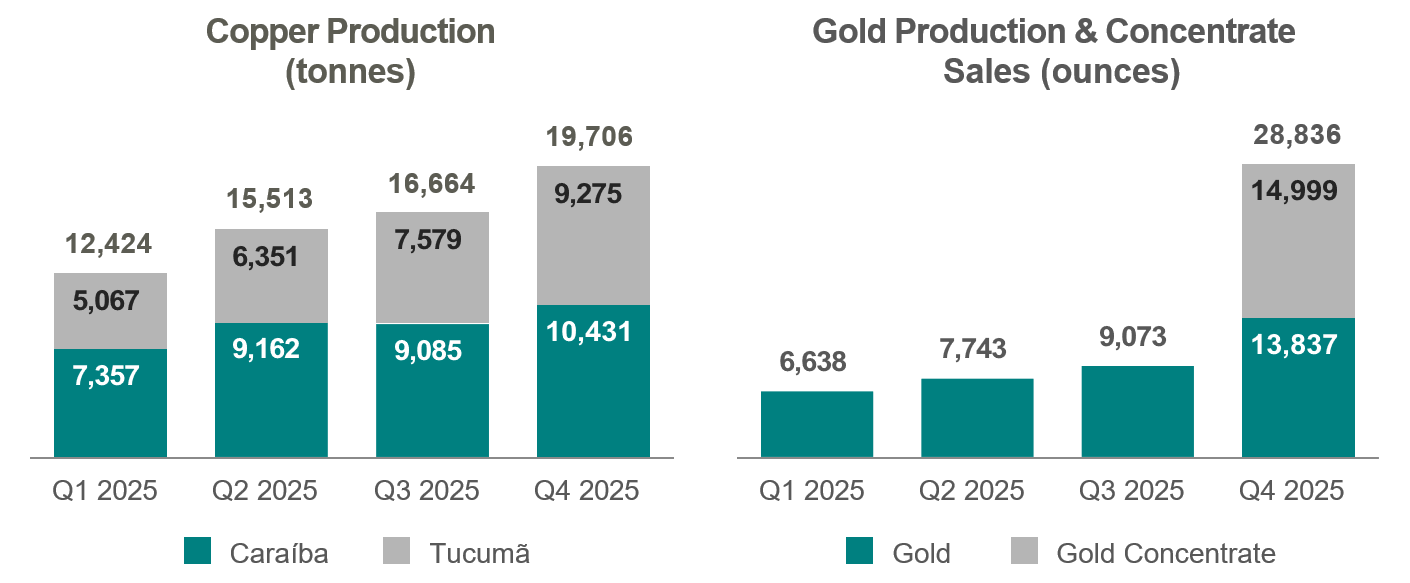

- Optimization initiatives across the Company's operating portfolio in 2025 contributed to record quarterly copper production of 19,706 tonnes and quarterly gold production of 13,837 ounces, representing production improvements of nearly

60% and more than100% compared to Q1 for copper and gold, respectively. - An additional 14,999 ounces of gold in concentrates were sold from the Xavantina Operations during Q4, the result of a year-long value-creation initiative that is expected to continue to augment gold production through mid-2027.

- Record full-year consolidated copper production of 64,307 tonnes, combined with gold production and gold from concentrate sales totaling 52,290 ounces, contributed to a quarter-on-quarter increase in liquidity of nearly

$40 million . As a result, year-end liquidity totaled approximately$150 million .(1)

- In 2025, the Company completed nearly 50,000 meters of exploration drilling at the Furnas Copper-Gold Project ("Furnas") and expects to publish the first preliminary economic assessment on the project in H1 2026. A further 50,000 meters of exploration drilling is planned in 2026 in support of accelerated engineering studies.

(1) Available liquidity as of December 31, 2025 includes approximately

2026 Guidance

- Consolidated copper production is expected to be in the range of 67,500 to 77,500 tonnes, representing an increase of up to

20% compared to 2025. Guidance reflects higher sustained plant throughput and lower planned grades at both Caraíba and Tucumã. Consolidated C1 cash costs are expected to be between$2.15 and$2.35 per pound of copper produced. - At the Xavantina Operations, gold production from mine operations is expected to total 40,000 to 50,000 ounces representing an increase of up to

34% compared to 2025, with C1 cash costs of$1,000 t o$1,250 per ounce of gold produced and all-in sustaining costs ("AISC") of$2,000 t o$2,500 per ounce produced. In addition, gold sales from the Xavantina Operations are expected to be significantly bolstered with the continued sale of gold concentrates that commenced in Q4 2025, and which are expected to continue through mid-2027. - Capital expenditures across the Company's operating portfolio are expected to range between

$245 and$280 million . This includes capital for additional mine ventilation, development, and equipment to support future growth at the Xavantina Operations, as well as approximately$80 million related to the continued construction of the Pilar Mine's new shaft and ancillary infrastructure at the Caraíba Operations. - The Company expects to spend an additional

$30 t o$40 million to continue advancing Furnas exploration, engineering, and permitting workstreams, and to further advance several exploration opportunities within the Company's portfolio.

Three-Year Production Outlook

- Consolidated copper production is expected to grow over the next three years, reaching between 80,000 and 90,000 tonnes by 2028.

- At the Caraíba Operations, plant debottlenecking completed in 2025 is expected to support higher sustained throughput levels going forward, accommodating increased ore tonnage from the Surubim Mine in 2026 and from the Pilar Mine's Deepening Extension Zone beginning in 2027.

- Copper production at the Tucumã Operation is expected to remain relatively steady through 2028, reflecting higher throughput levels, lower planned grades, and an improved stockpile management framework that is expected to reduce rehandle costs over the outlook period.

- Xavantina's mining and processing operations are projected to deliver higher sustained production of between 50,000 and 60,000 ounces in 2027 and 2028, driven by the transition to mechanized mining and further utilization of excess plant capacity. The Company also expects sales of gold concentrates to continue through mid-2027.

“2025 marked a year of meaningful investment and transformative progress throughout the Company. We worked to strengthen our health and safety performance while executing on several key initiatives that are supporting higher sustained mining and processing rates across our operations. These efforts included the transition to mechanized mining at Xavantina, the successful completion of a multi-quarter debottlenecking effort at Caraíba and the continued ramp-up of Tucumã. The success of these programs resulted in significant quarter-on-quarter growth throughout 2025. In parallel, we completed a year-long value-creation initiative that culminated in the commencement of gold concentrate sales at Xavantina, with nearly 15,000 ounces sold in the fourth quarter," said Makko DeFilippo, President & Chief Executive Officer.

"Looking ahead, we expect to deliver steady growth across our portfolio as we advance longer-term growth initiatives, including the new shaft at the Pilar Mine and the delivery of what will be the first preliminary economic assessment ever published on the Furnas Project. Entering 2026 with a strengthening balance sheet, combined with what we fully expect will be a record year of copper production and record gold sales - including ongoing gold concentrate sales at Xavantina - has positioned Ero's shareholders to benefit from this historic commodity price environment."

FOURTH QUARTER AND FULL-YEAR 2025 PRODUCTION RESULTS

| Q4 2025 | Full Year 2025 | |

| Caraíba Operations | ||

| Tonnes Processed | 1,174,732 | 3,656,240 |

| Grade (% Cu) | 1.00 | 1.09 |

| Recovery Rate (%) | 88.7 | 90.0 |

| Copper Production (tonnes) | 10,431 | 36,035 |

| Tucumã Operation | ||

| Tonnes Processed | 517,246 | 1,805,300 |

| Grade (% Cu) | 1.93 | 1.79 |

| Recovery Rate (%) | 90.5 | 88.7 |

| Copper Production (tonnes) | 9,275 | 28,272 |

| Consolidated Copper Production (tonnes) | 19,706 | 64,307 |

| Xavantina Operations | ||

| Tonnes Processed | 53,256 | 172,178 |

| Grade (gpt Au) | 9.98 | 8.24 |

| Recovery Rate (%) | 79.6 | 82.8 |

| Au Production (ounces) | 13,837 | 37,291 |

| Gold Concentrate Sales | ||

| Tonnes Invoiced | 14,614 | 14,614 |

| Grade (gpt Au) | 31.92 | 31.92 |

| Contained Gold (ounces) | 14,999 | 14,999 |

| Total Gold (ounces) | 28,836 | 52,290 |

Record quarterly and full-year consolidated copper production reflect strong operational execution across the portfolio, including the continued ramp-up of the Tucumã Operation and the achievement of record mill throughput at the Caraíba Operations following the successful completion of a plant debottlenecking initiative during the year.

At Tucumã, production increased sequentially each quarter in 2025, with Q4 representing the strongest quarter to date, producing 9,275 tonnes of copper in concentrate, representing a quarter-on-quarter increase of approximately

Caraíba also delivered its strongest production quarter of the year, supported by record quarterly mill throughput, which offset the impact of lower-than-planned mined and processed grades related to timing of stope sequencing, higher-than-planned operational dilution in select stopes during the quarter, and unplanned downtime in the crusher circuit that occurred late in the year. As a result, production increased

At Xavantina, gold production increased sequentially throughout 2025, highlighted by a significant

2026 PRODUCTION GUIDANCE AND THREE-YEAR PRODUCTION OUTLOOK

The Company's 2026 guidance and three-year production outlook reflect consistent growth relative to 2025. Key drivers in 2026 include higher plant throughput across the operations, supported by the Caraíba mill debottlenecking initiative successfully completed in 2025, and projected increases in throughput at the Tucumã Operation toward steady-state levels. Longer term, copper production growth is expected to be supported by planned increases in tailings filtration capacity at Tucumã and the new shaft at the Caraíba Operations' Pilar Mine, which is expected to become operational in 2027. As a result, consolidated copper production is expected to increase over the next three years to between 80,000 and 90,000 tonnes by 2028.

At the Xavantina Operations, annual gold production is expected to increase from between 40,000 and 50,000 ounces in 2026 to between 50,000 and 60,000 ounces in 2027 and 2028, driven by higher mine production and increased mill throughput supported by the transition to mechanized mining. In addition, gold sales from the Xavantina Operations are expected to be significantly bolstered with the continued sale of gold concentrates that commenced in Q4 2025, and which are expected to continue through mid-2027.

| 2026 | 2027 | 2028 | |

| Copper (tonnes) | |||

| Caraíba Operations | 35,000 - 40,000 | 40,000 - 45,000 | 45,000 - 50,000 |

| Tucumã Operation | 32,500 - 37,500 | 35,000 - 40,000 | 35,000-40,000 |

| Total Copper | 67,500 - 77,500 | 75,000 - 85,000 | 80,000 - 90,000 |

| Gold (ounces) | |||

| Xavantina Operations | 40,000 - 50,000 | 50,000 - 60,000 | 50,000 - 60,000 |

| Gold in Concentrates(1) | Concentrate sales expected to continue through mid-2027(1) | ||

Note: Guidance is based on estimates and assumptions including, but not limited to, mineral resource and reserve estimates, grade and continuity of interpreted geological formations and metallurgical recovery performance. Please refer to the Company’s SEDAR+ and EDGAR filings, including the most recent Annual Information Form ("AIF"), for a detailed summary of risk factors.

(1) Gold concentrate sales over the projection period related to Xavantina's stockpiled gold concentrate remain subject to ongoing sampling.

2026 COST GUIDANCE

2026 copper C1 cash cost guidance on a consolidated basis is

At the Xavantina Operations, the C1 cash cost guidance range for ounces produced from mining and processing operations is

| Copper C1 Cash Cost ($/lb) | |

| Caraíba Operations | |

| Tucumã Operation | |

| Consolidated Copper Operations | |

| Gold C1 Cash Cost ($/oz) | |

| Gold All-In Sustaining Cost ($/oz) | |

Note: C1 Cash Costs and AISC are non-IFRS measures. Please see the Notes section of this press release for additional information.

2026 CAPITAL EXPENDITURE GUIDANCE

Total capital expenditures in 2026 are expected to range between

Figures presented below are in USD millions.

| Caraíba Operations | |

| Tucumã Operation | |

| Xavantina Operations | |

| Furnas Copper-Gold Project, Other Exploration & Corporate | |

| Total | |

QUALIFIED PERSONS AND THE NI 43-101 TECHNICAL REPORT

Mr. Cid Gonçalves Monteiro Filho, SME RM (04317974), MAIG (No. 8444), FAusIMM (No. 329148) has reviewed, verified and approved the scientific and technical information contained in this press release, including the sampling, analytical and test data underlying the information contained in this press release. Mr. Monteiro is Manager, Resources & Reserves of the Company and is a “qualified person” within the meanings of NI 43-101.

NOTES

Alternative Performance (Non-IFRS) Measures

The Company utilizes certain alternative performance (non-IFRS) measures to monitor its performance, including C1 cash cost of copper produced (per lb), C1 cash cost of gold produced (per ounce), and AISC of gold produced (per ounce). These performance measures have no standardized meaning prescribed within generally accepted accounting principles under IFRS and, therefore, amounts presented may not be comparable to similar measures presented by other mining companies. These non-IFRS measures are intended to provide supplemental information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS.

C1 Cash Cost of Copper Produced (per lb)

C1 cash cost of copper produced (per lb) is a non-IFRS performance measure used by the Company to manage and evaluate the operating performance of its copper mining segment and is calculated as C1 cash costs divided by total pounds of copper produced during the period. C1 cash costs comprise the total cost of production, including expenses related to transportation, and treatment and refining charges. These costs are net of by-product credits and incentive payments.

While the C1 cash cost of copper produced per pound is widely reported in the mining industry as a performance benchmark, it does not have a standardized meaning and is disclosed as a supplement to IFRS measures.

C1 Cash Cost of Gold produced (per ounce) and AISC of Gold produced (per ounce)

C1 cash cost of gold produced (per ounce) is a non-IFRS performance measure used by the Company to manage and evaluate the operating performance of its gold mining segment and is calculated as C1 cash costs divided by total ounces of gold produced during the period. C1 cash cost includes total cost of production, net of by-product credits and incentive payments. C1 cash cost of gold produced per ounce is widely reported in the mining industry as benchmarks for performance but does not have a standardized meaning and is disclosed in supplemental to IFRS measures.

AISC of gold produced (per ounce) is an extension of C1 cash cost of gold produced (per ounce) discussed above and is also a key performance measure used by management to evaluate operating performance of its gold mining segment. AISC of gold produced (per ounce) is calculated as AISC divided by total ounces of gold produced during the period. AISC includes C1 cash costs, site general and administrative costs, accretion of mine closure and rehabilitation provision, sustaining capital expenditures, sustaining leases, and royalties and production taxes. AISC of gold produced (per ounce) is widely reported in the mining industry as benchmarks for performance but does not have a standardized meaning and is disclosed in supplement to IFRS measures.

ABOUT ERO

Ero is a Brazil-focused, growth-oriented mining company with a diversified portfolio of copper and gold assets. Headquartered in Vancouver, B.C., the Company operates two copper mines – the Caraíba Operations in Bahia State and the Tucumã Operation in Pará State – as well as the Xavantina Operations, a producing gold mine in Mato Grosso State. In addition to its operating assets, Ero is advancing the Furnas Copper-Gold Project, located in the mineral-rich Carajás Province in Pará State, through a definitive earn-in agreement with Vale Base Metals to acquire a

Ero’s operating philosophy is grounded in a commitment to safety, operational excellence, and the responsible production of minerals essential for a better tomorrow. The Company’s shares are publicly traded on the Toronto Stock Exchange and the New York Stock Exchange under the symbol “ERO.” Additional information, including technical reports on the Company’s operations and projects, is available on the Company’s website (www.ero.com), SEDAR+ (www.sedarplus.ca), and on EDGAR (www.sec.gov).

FOR MORE INFORMATION, PLEASE CONTACT

Farooq Hamed, VP, Investor Relations

info@ero.com

CAUTION REGARDING FORWARD LOOKING INFORMATION AND STATEMENTS

This press release contains “forward-looking statements” within the meaning of the United States Private Securities Litigation Reform Act of 1995 and “forward-looking information” within the meaning of applicable Canadian securities legislation (collectively, “forward-looking statements”). Forward-looking statements include statements that use forward-looking terminology such as “may”, “could”, “would”, “will”, “should”, “intend”, “target”, “plan”, “expect”, “budget”, “estimate”, “forecast”, “schedule”, “anticipate”, “believe”, “continue”, “potential”, “view” or the negative or grammatical variation thereof or other variations thereof or comparable terminology. Forward-looking statements may include, but are not limited to, statements with respect to the Company's expected development and mining rates, production, operating costs and capital expenditures at the Caraíba Operations, the Tucumã Operation and the Xavantina Operations; estimated timing for certain milestones and the potential impacts of previously completed initiatives, including the ramp-up of throughput volumes at the Tucumã Operation; the completion cost and estimated operating timeline of the Pilar Mine's new shaft at the Caraíba Operations; the expected contributions from the Surubim Mine; the expected cost reductions associated with rehandle optimization work at Tucumã; the timing of the preliminary economic analysis on Furnas; the ability of the Company to sustain higher copper and gold production levels in 2027 and 2028; the Company's ability to monetize gold concentrates produced at the Xavantina Operations, including expectations for the volume, gold grades, timing, and/or potential value of gold concentrates sold; the future strength of the Company's balance sheet which is dependent on operational performance as well as external factors including prevailing commodity prices; the amount of exploration drilling and ability to execute on engineering and permitting milestones, as well as the Company's ability to advance work programs under the Furnas earn-in agreement; and any other statement that may predict, forecast, indicate or imply future plans, intentions, levels of activity, results, performance or achievements.

Forward-looking statements are subject to a variety of known and unknown risks, uncertainties and other factors that could cause actual results, actions, events, conditions, performance or achievements to materially differ from those expressed or implied by the forward-looking statements, including, without limitation, risks discussed in this press release and in the Company’s most recent Annual Information Form (“AIF”) under the heading “Risk Factors”. The risks discussed in this press release and in the AIF are not exhaustive of the factors that may affect any of the Company’s forward-looking statements. Although the Company has attempted to identify important factors that could cause actual results, actions, events, conditions, performance or achievements to differ materially from those contained in forward-looking statements, there may be other factors that cause results, actions, events, conditions, performance or achievements to differ from those anticipated, estimated or intended.

Forward-looking statements are not a guarantee of future performance. There can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Forward-looking statements involve statements about the future and are inherently uncertain, and the Company’s actual results, achievements or other future events or conditions may differ materially from those reflected in the forward-looking statements due to a variety of risks, uncertainties and other factors, including, without limitation, those referred to herein and in the AIF under the heading “Risk Factors”.

The Company’s forward-looking statements are based on the assumptions, beliefs, expectations and opinions of management on the date the statements are made, many of which may be difficult to predict and beyond the Company’s control. In connection with the forward-looking statements contained in this press release and in the AIF, the Company has made certain assumptions about, among other things: favourable equity and debt capital markets; the ability to raise any necessary additional capital on reasonable terms to advance the production, development and exploration of the Company’s properties and assets; future prices of copper, gold and other metal prices; the timing and results of exploration and drilling programs; the accuracy of any mineral reserve and mineral resource estimates; the geology of the Caraíba Operations, the Xavantina Operations, the Tucumã Operation and the Furnas Copper-Gold Project being as described in the respective technical report for each property; production costs; the accuracy of budgeted exploration, development and construction costs and expenditures; the price of other commodities such as fuel; future currency exchange rates, interest rates and tariff rates; operating conditions being favourable such that the Company is able to operate in a safe, efficient and effective manner; work force continuing to remain healthy in the face of prevailing epidemics, pandemics or other health risks, political and regulatory stability; the receipt of governmental, regulatory and third party approvals, licenses and permits on favourable terms; obtaining required renewals for existing approvals, licenses and permits on favourable terms; requirements under applicable laws; sustained labour stability; stability in financial and capital goods markets; availability of equipment; positive relations with local groups and the Company’s ability to meet its obligations under its agreements with such groups; and satisfying the terms and conditions of the Company’s current loan arrangements. Although the Company believes that the assumptions inherent in forward-looking statements are reasonable as of the date of this press release, these assumptions are subject to significant business, social, economic, political, regulatory, competitive and other risks and uncertainties, contingencies and other factors that could cause actual actions, events, conditions, results, performance or achievements to be materially different from those projected in the forward-looking statements. The Company cautions that the foregoing list of assumptions is not exhaustive. Other events or circumstances could cause actual results to differ materially from those estimated or projected and expressed in, or implied by, the forward-looking statements contained in this press release. There can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements.

Forward-looking statements contained herein are made as of the date of this press release and the Company disclaims any obligation to update or revise any forward-looking statement, whether as a result of new information, future events or results or otherwise, except as and to the extent required by applicable securities laws.

CAUTIONARY NOTES REGARDING MINERAL RESOURCE AND MINERAL RESERVE ESTIMATES

Unless otherwise indicated, all reserve and resource estimates included in this press release and the documents incorporated by reference herein have been prepared in accordance with National Instrument 43-101, Standards of Disclosure for Mineral Projects (“NI 43-101") and the Canadian Institute of Mining, Metallurgy and Petroleum (the “CIM”) — CIM Definition Standards on Mineral Resources and Mineral Reserves, adopted by the CIM Council, as amended (the “CIM Standards”). NI 43-101 is a rule developed by the Canadian Securities Administrators that establishes standards for all public disclosure an issuer makes of scientific and technical information concerning mineral projects. Canadian standards, including NI 43-101, differ significantly from the requirements of the United States Securities and Exchange Commission (the “SEC”), and reserve and resource information included herein may not be comparable to similar information disclosed by U.S. companies. In particular, and without limiting the generality of the foregoing, this press release and the documents incorporated by reference herein use the terms “measured resources,” “indicated resources” and “inferred resources” as defined in accordance with NI 43-101 and the CIM Standards.

A figure accompanying this announcement is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/f98adeb1-2864-4ea0-940b-eb1419d803ab