Spending power improvements a positive sign, yet financial recovery still underway

DULUTH, Ga.--(BUSINESS WIRE)--

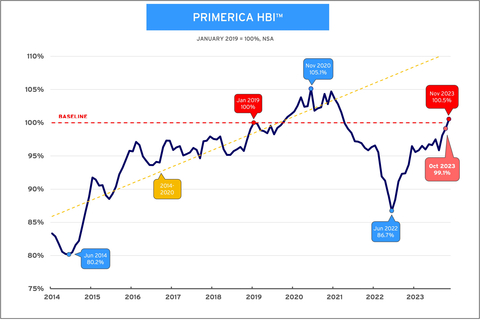

Primerica, Inc. (NYSE: PRI), a leading provider of financial services in the United States and Canada, announced today the release of the Primerica Household Budget Index™ (HBI™), a monthly index illustrating the purchasing power of middle-income households with incomes between $30,000 and $130,000. In November 2023, the average purchasing power for middle-income households was 100.5%, up from 99.1% in October. A year ago, the index stood at 93.7%.

Primerica Household Budget Index™ (HBI™) - In November 2023, the average purchasing power for middle-income households was 100.5%, up from 99.1% in October. A year ago, the index stood at 93.7%. (Graphic: Business Wire)

“During November, a significant decrease in gasoline prices and a small decrease in food prices, accompanied by continued strength in household incomes, allowed middle-income families to stem the loss of purchasing power they have experienced for several consecutive months,” said Glenn J. Williams, CEO of Primerica. “These families have consistently indicated that the cost of living is weighing on their financial security.”

In November, HBI™data showed middle-income households saw modest improvements in spending power. However, since 2021, driven by the increased costs of necessity items, households experienced an average cumulative budget deficit of nearly $2,500.

“So much has happened since January 2019, and for the index to finally come back to the baseline value is a welcome outcome,” said Amy Crews Cutts, Ph.D., CBE®, economic consultant to Primerica. “But it doesn’t mean that all is grand. Had the pandemic never happened, the HBI™ would likely be approximately 10% higher than it is now, there would be more savings accumulation for middle-income households, and middle-income families would not be carrying all the new credit card debt they incurred when inflation was roaring well ahead of earned income.”

HBI™ HISTORICAL BACKGROUND

The index baseline is set at January 2019 and can be thought of as when middle-income households set a budget based on their earned income at that time. Between 2014 and 2020, the HBI™ results recorded steady gains in purchasing power for middle-income families, with a peak of 105.1% in November 2020. This means that relative to January 2019, households were in a stronger financial position to pay their monthly bills because wage growth outpaced the cost of everyday goods. Increasing inflation then caused the index to plummet. In June 2022, it reached a post-pandemic low of 86.7%.

Since May of 2021, when the HBI™ dipped below 100% for the first time since the pandemic, the average middle-income household has cumulatively spent around $2,425 more than budget on basic necessities. In line with this, if the pandemic and ensuing inflation would not have been a factor, the HBI™ today would be closer to 110%.

About the Primerica Household Budget Index™ (HBI™)

The Primerica Household Budget Index™ (HBI™) is constructed monthly on behalf of Primerica by its chief economic consultant Amy Crews Cutts, PhD, CBE®. The index measures the purchasing power of middle-income families with household incomes from $30,000 to $130,000 and is developed using data from the U.S. Bureau of Labor Statistics, the US Bureau of the Census, and the Federal Reserve Bank of Kansas City. The index looks at the cost of necessities including food, gas, utilities, and health care and earned income to track differences in inflation and wage growth.

The HBI™ is presented as a percentage. If the index is above 100%, the purchasing power of middle-income families is stronger than in the baseline period and they may have extra money left over at the end of the month that can be applied to things like entertainment, extra savings, or debt reduction. If it is under 100%, households may have to reduce overall spending to levels below budget, reduce their savings or increase debt to cover expenses. The HBI™ uses January 2019 as its baseline. This point in time reflects a recent “normal” economic time prior to the COVID-19 pandemic.

Periodically, prior HBI™ values may be revised due to revisions in the CPI series and Consumer Expenditure Survey releases by the U.S. Bureau of Labor Statistics (BLS). Beginning with the October 2023 release of the HBI™ data, health insurance costs will no longer be included in the calculation of the HBI™ data as part of the healthcare component because of some newly acknowledged methodology that has been used by the BLS to calculate the health insurance CPI. The health insurance CPI, as calculated by BLS, does not measure consumer costs of health insurance such as the cost of premiums paid or a combination of premiums and deductibles, but rather premium values retained by health insurers we do not believe it accurately reflects consumer experiences. The healthcare component will continue to include medical services, prescription drugs and equipment. Prior published values have been adjusted to reflect this change.

About Primerica, Inc.

Primerica, Inc., headquartered in Duluth, GA, is a leading provider of financial products and services to middle-income households in North America. Independent licensed representatives educate Primerica clients about how to better prepare for a more secure financial future by assessing their needs and providing appropriate solutions through term life insurance, which we underwrite, and mutual funds, annuities and other financial products, which we distribute primarily on behalf of third parties. We insured over 5.7 million lives and had over 2.8 million client investment accounts on December 31, 2022. Primerica, through its insurance company subsidiaries, was the #3 issuer of Term Life insurance coverage in the United States and Canada in 2022. Primerica stock is included in the S&P MidCap 400 and the Russell 1000 stock indices and is traded on The New York Stock Exchange under the symbol “PRI”.