S&P Global Market Intelligence U.S. Bank Market Report Finds Earnings are Expected to Fall 2.8% year-over-year in 2024, but Rebound Strongly in 2025

"Even as interest rates are expected to fall in the second half of 2024, deposits remain firmly in focus for

Earnings should rebound strongly for most institutions in 2025 and 2026 as institutions weather the credit cycle, absorb losses and record lower provisions for loan losses. This in turn could bring many investors back to the banking group, and banks whose credit quality outperforms others should attract even greater investor interest as they will boast even stronger earnings streams that allow them to play offense through organic growth and by using their superior currency for acquisitions.

Key highlights from the report include:

- Fierce deposit competition should persist amid regulatory pressures and higher-for-longer interest rates as banks place a higher value on deposits than other forms of funding.

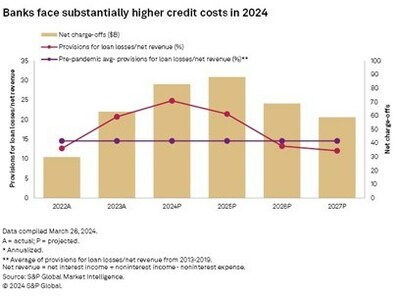

- Bank credit quality is expected to weaken in 2024 and 2025, led by higher delinquencies and losses in the commercial real estate (CRE) portfolios, but the deterioration will serve as a hit to earnings rather than a threat to safety and soundness for most institutions.

- Regulators have reiterated the importance of banks maintaining strong risk management of their CRE portfolios, particularly for institutions with elevated CRE concentrations. In some cases, regulators have imposed independent minimum capital requirements for banks with elevated CRE concentrations.

U.S. bank earnings are expected to rebound strongly in 2025 and 2026 as provisions for loan losses decline and become a much smaller headwind to earnings.

To request a copy of the 2024 U.S. Bank Market Report, please contact press.mi@spglobal.com.

S&P Global Market Intelligence's opinions, quotes, and credit-related and other analyses are statements of opinion as of the date they are expressed and not statements of fact or recommendation to purchase, hold, or sell any securities or to make any investment decisions, and do not address the suitability of any security.

About S&P Global Market Intelligence

At S&P Global Market Intelligence, we understand the importance of accurate, deep and insightful information. Our team of experts delivers unrivaled insights and leading data and technology solutions, partnering with customers to expand their perspective, operate with confidence, and make decisions with conviction.

S&P Global Market Intelligence is a division of S&P Global (NYSE: SPGI). S&P Global is the world's foremost provider of credit ratings, benchmarks, analytics and workflow solutions in the global capital, commodity and automotive markets. With every one of our offerings, we help many of the world's leading organizations navigate the economic landscape so they can plan for tomorrow, today. For more information, visit www.spglobal.com/marketintelligence.

Media Contact

Katherine Smith

S&P Global Market Intelligence

+1 781 301 9311

katherine.smith@spglobal.com

![]()

![]() View original content to download multimedia:https://www.prnewswire.com/news-releases/sp-global-market-intelligence-us-bank-market-report-finds-earnings-are-expected-to-fall-2-8-year-over-year-in-2024--but-rebound-strongly-in-2025--302117149.html

View original content to download multimedia:https://www.prnewswire.com/news-releases/sp-global-market-intelligence-us-bank-market-report-finds-earnings-are-expected-to-fall-2-8-year-over-year-in-2024--but-rebound-strongly-in-2025--302117149.html

SOURCE S&P Global Market Intelligence