B2Gold Announces Positive Preliminary Economic Assessment Results for the Gramalote Project; After-Tax NPV (5%) of $778 Million with an After-Tax IRR of 20.6%

Rhea-AI Summary

B2Gold has reported positive preliminary economic assessment (PEA) results for its 100%-owned Gramalote gold project in Antioquia, Colombia. The PEA reveals an after-tax net present value (NPV) of $778 million at a 5% discount rate, and an after-tax internal rate of return (IRR) of 20.6%. The project is expected to generate an after-tax free cash flow of $1.38 billion over its life. The open pit mine has an initial life of 10 years, processing gold over 12.5 years, and anticipates producing 2.3 million ounces of gold with an average recovery rate of 95.9%. The initial five years will see an average annual gold production of 234,000 ounces. The project’s all-in sustaining costs (AISC) are projected to be $886 per ounce. Pre-production capital costs are estimated at $807 million. B2Gold plans to begin feasibility work, aiming to complete a feasibility study by mid-2025. The project benefits from robust infrastructure, local support, and promising metallurgical characteristics.

Positive

- After-tax NPV of $778 million.

- After-tax IRR of 20.6%.

- Estimated after-tax free cash flow of $1.38 billion.

- Initial gold production of 234,000 ounces per year for the first five years.

- Projected AISC of $886 per gold ounce.

- Life of Project gold production of approximately 2.3 million ounces.

- High gold recovery rate of 95.9%.

- Robust historical drilling with over 270,000 meters completed.

- Existing mining permit in place.

- Strong local community and government support.

Negative

- Estimated pre-production capital cost of $807 million.

- The project requires modification of the existing permit, with anticipated time frame of 12-18 months.

- PEA includes speculative Inferred Mineral Resources with no guaranteed economic viability.

- Sensitive to gold price fluctuations, with significant variance in NPV and IRR.

News Market Reaction – BTG

In the trading session that priced this news, BTG gained 3.50%, reflecting a moderate positive market reaction.

Data tracked by StockTitan Argus on the day of publication.

AI-generated analysis. How Rhea-AI works. Not financial advice.

VANCOUVER, British Columbia, June 18, 2024 (GLOBE NEWSWIRE) -- B2Gold Corp. (TSX: BTO, NYSE AMERICAN: BTG, NSX: B2G) (“B2Gold” or the “Company”) is pleased to announce the results of a positive Preliminary Economic Assessment (“PEA”) prepared in accordance with National Instrument 43-101 (“NI 43-101”) on its

Highlights

- Significant gold production profile with low-cost structure and favorable metallurgical characteristics

- Open pit gold mine with an initial life of mine of 10 years, with mill processing over 12.5 years (“Life of Project”)

- Average grade processed of 1.26 grams per tonne (“g/t”) gold over the first five years, benefitting from the processing of the higher-grade core at the Gramalote Project; Life of Project average grade processed of 1.00 g/t gold

- Life of Project gold production of approximately 2.3 million ounces with an average gold recovery of

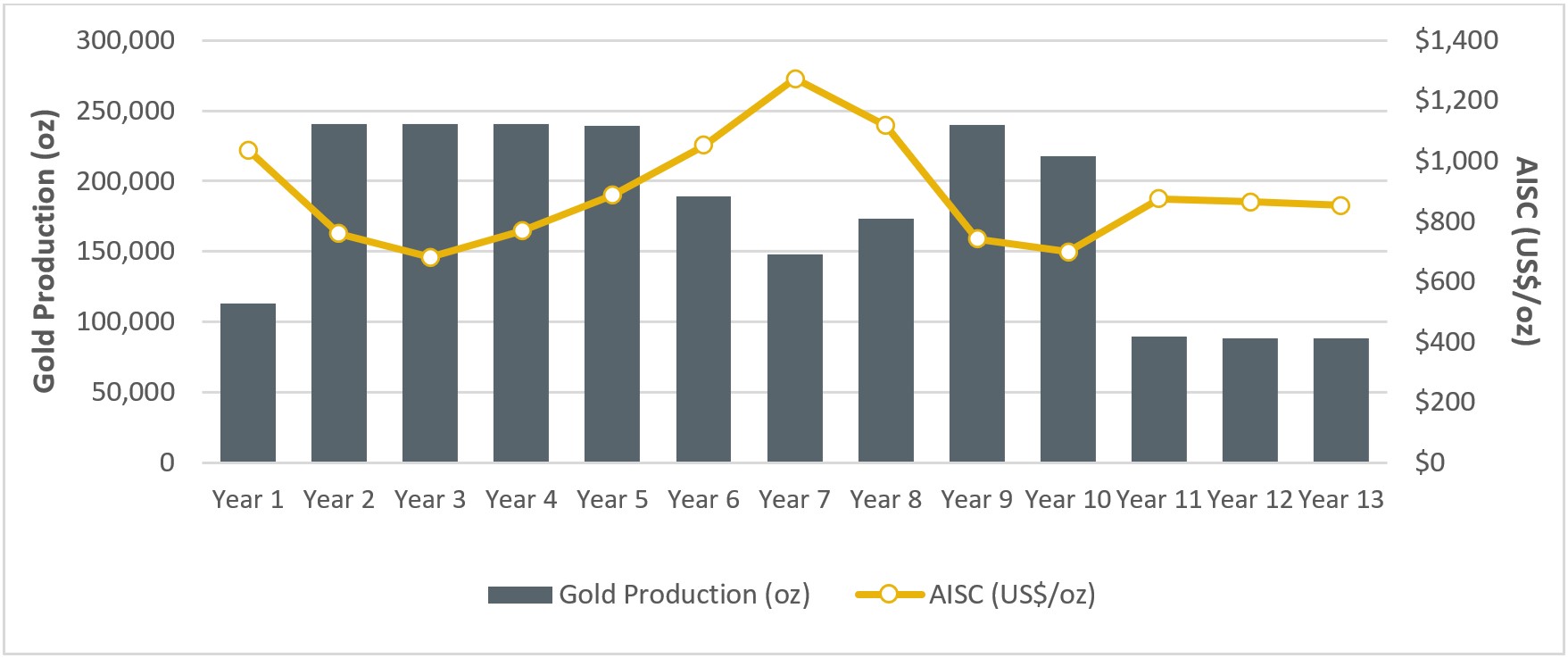

95.9% from conventional milling, flotation and cyanide leach of the flotation concentrate - Average annual gold production of approximately 234,000 ounces per year for the first five years of production

- Average annual gold production of approximately 185,000 ounces per year over the Life of Project

- Projected lowest quartile all-in sustaining costs (“AISC”) of

$886 per gold ounce over the Life of Project - Annual processing rate of 6.0 million tonnes per annum (“Mtpa”)

- Strong project economics

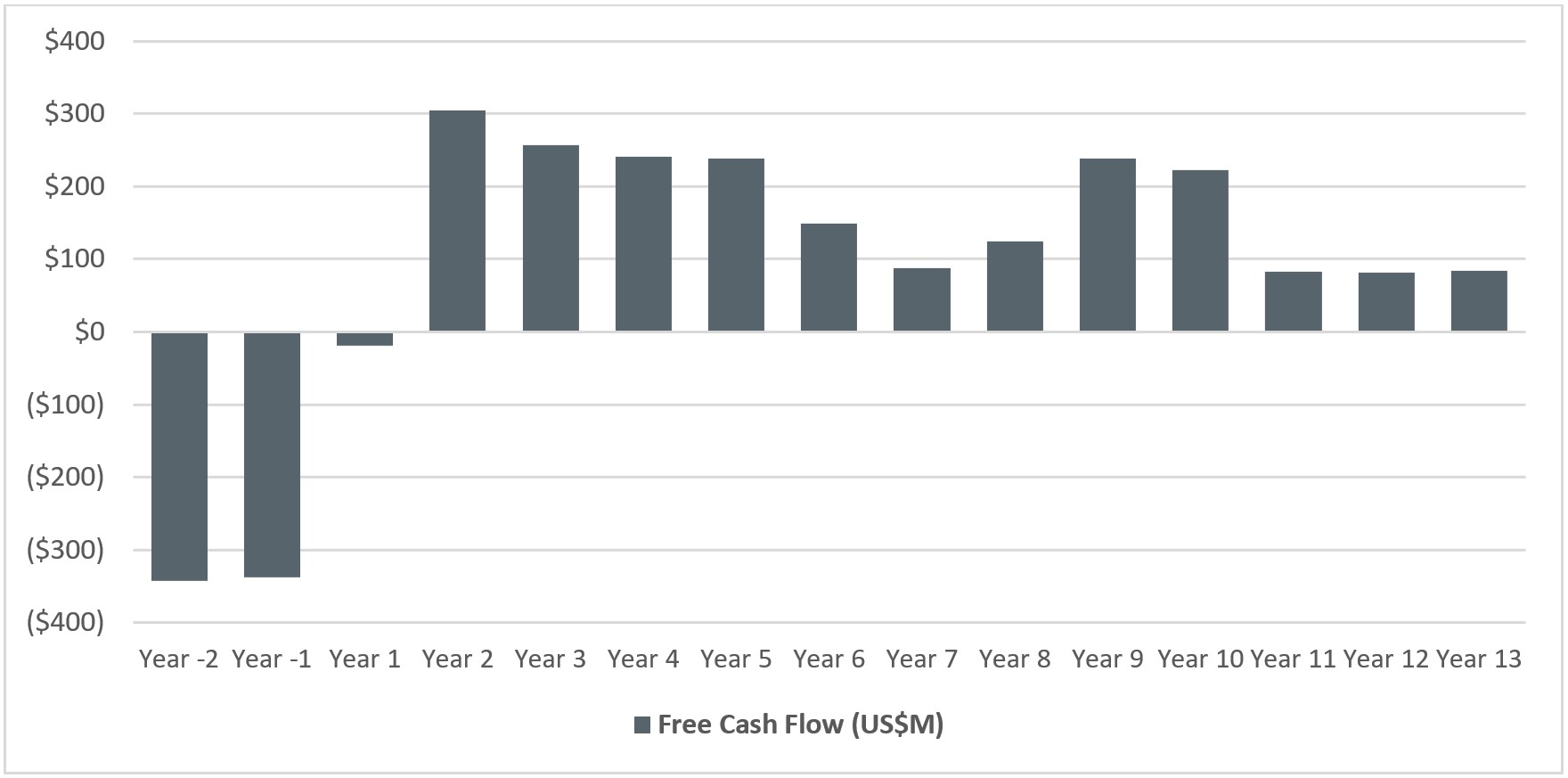

- Life of Project after-tax free cash flow of

$1.38 billion - Assuming a discount rate of

5.0% , net present value (“NPV”) after-tax of$778 million , generating an after-tax internal rate of return (“IRR”) of20.6% , with a project payback on pre-production capital of 3.1 years - Estimated pre-production capital cost of

$807 million (includes approximately$93 million for mining equipment and$63 million for contingency)

- Life of Project after-tax free cash flow of

- Robust amount of historical drilling and engineering studies have been completed on Gramalote, which significantly de-risks future project development

- Over 270,000 meters of historical drilling, providing B2Gold with a robust mineral resource model

- Gramalote has a long history of studies and technical reports which supported the existing mining permit that is currently in place

- As well, specific mining, processing, infrastructure, environmental, and social studies have been historically completed. Extensive metallurgical test work has demonstrated high gold recoveries (approximately

96% ) at a coarse grind size for the selected processing flow sheet. This provides a high level of confidence in the engineering, production and operating cost estimates contained in the PEA

- Gramalote benefits from strong local community and government support

- An existing mining permit is currently in place on a larger-scale project; this permit will require modification to reflect the new medium-scale project contemplated in the PEA

- B2Gold anticipates the permit modification time frame will be between 12 and 18 months from submission to the permit authorities

- B2Gold to commence feasibility work with the goal of completing a feasibility study by mid-2025

PEA Overview

The Gramalote Project is located in central Colombia, approximately 230 kilometers (“km”) northwest of Bogota and 100 km northeast of Medellin, in the Province of Antioquia, which has expressed a positive attitude towards the development of responsible mining projects in the region. Based on the preliminary results completed in 2022 of the contemplated large-scale project with AngloGold Ashanti Limited (“AngloGold”), the project did not meet the combined investment return thresholds for development by both

The PEA, with an effective date of April 1, 2024, was prepared by B2Gold and evaluates recovery of gold from an open pit mining operation that will move up to approximately 97,000 tonnes per day (“tpd”) (35.3 Mtpa), with an approximately 16,500 tpd (6.0 Mtpa) processing plant that includes crushing, grinding, flotation, with fine grinding of the flotation concentrate and agitated leaching of the flotation concentrate followed by a carbon-in-pulp recovery process to process doré bullion. The Mineral Resource estimate for the Gramalote Project that forms the basis for the PEA includes Indicated Mineral Resources of 192.2 million tonnes grading 0.68 g/t gold for a total of 4,210,000 ounces of gold and Inferred Mineral Resources of 85.4 million tonnes grading 0.54 g/t gold for a total of 1,480,000 ounces of gold.

The PEA assumptions include revenues using a gold price of

Table 1 - Key Parameters of the PEA

| First Five Years | Life of Project | |

| Production Profile | ||

| Years | 5.0 | 12.5 |

| Ore tonnes processed (Mt) | 30.0 | 75.0 |

| Average gold grade processed (g/t) | 1.26 | 1.00 |

| Gold recovery (%) | 96.2 | 95.9 |

| Gold ounces produced (oz) | 1,169,000 | 2,309,000 |

| Average annual gold production (oz) | 234,000 | 185,000 |

| Operating Costs | ||

| Cash operating costs1 ($/oz gold) | 510 | 622 |

| All-In Sustaining Costs2 ($/oz gold) | 822 | 886 |

| Mining cost ($/t mined) | 2.25 | 2.40 |

| Processing cost ($/t processed) | 7.76 | 7.82 |

| General & administration ($/t processed) | 3.03 | 3.49 |

| Capital Costs | ||

| Pre-production capital ($M) | 807 | |

| Sustaining capital ($M) | 364 | |

Notes:

- Cash operating costs consist of mining costs, processing costs and site G&A.

- AISC consist of cash operating costs, royalties, corporate G&A, selling costs and silver credits and excluding pre-production capital costs.

Table 2 – Pre-Production Capital Estimate

| ($M) | |

| Mining pre-strip | 19 |

| Tailings storage facility | 28 |

| Process plant | 263 |

| Mining equipment | 93 |

| Infrastructure (roads, platform, river diversion, camp, etc.) | 177 |

| Owners / management cost | 103 |

| Other (resettlement, general, light vehicles) | 62 |

| Subtotal | 745 |

| Contingency | 63 |

| Total | 807 |

Table 3 – Project Economics Summary

| After-Tax | |

| NPV | 778 |

| IRR (%) | |

| Payback (years) | 3.1 |

| Free cash flow ($M) | 1,376 |

Note:

- NPV

5.0% is calculated as of the start of construction expenditure.

Chart 1 – Production and Cost Profile by Year

Chart 1 is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/680c2185-d513-4d95-985e-59703a8f968b

Chart 2 – Free Cash Flow by Year

Chart 2 is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/c36f5d82-6d51-4044-a7aa-6d1918619eaa

Based on the positive results from the PEA, B2Gold believes that the Gramalote Project has the potential to become a medium-scale, low-cost, open pit gold mine. The Gramalote Project has several key infrastructure advantages, including:

- Reliable water supply – high rainfall region and located next to the Nus River

- Adjacent to a national highway, which connects directly to Medellin and to a major river with port facilities, capable of bringing supplies by barge to within 70 km of the site

- Skilled labour workforce within Colombia

In addition, B2Gold expects the Gramalote Project to benefit from several key operational advantages, including:

- Excellent metallurgical characteristics of the ore, which results in high recovery rates at low processing costs

- Relatively low strip ratio (3.3:1 strip ratio over the Life of Project)

- Ability to mine and process higher-grade ore in the initial years of the mine life resulting in improved project economics

The PEA is subject to a number of assumptions and risks, including among others that a Modified Environmental Impact Study will be approved, all required permits, permit amendments and other rights will be obtained in a timely manner, the Gramalote Project will have the support of the local government and community, the regulatory environment will remain consistent, that Gramalote can operate under a single company free trade zone in Colombia, and no material increase will have occurred to the estimated costs.

The PEA is preliminary in nature and includes a small amount of Inferred Mineral Resources that are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorized as Mineral Reserves, and there is no certainty that the PEA based on these Mineral Resources will be realized. Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability.

Economic Sensitivities

Gramalote is a medium-scale, low operating cost project and sensitive to the gold price, as demonstrated in the following table:

Table 4 – Economic Sensitivity to Long-Term Gold Price

| Long-Term Gold Price ($/oz) | After-Tax NPV ($M) | After-Tax IRR (%) | |

| 310 | 12.0 | ||

| 544 | 16.5 | ||

| 778 | 20.6 | ||

| 1,012 | 24.4 | ||

| 1,246 | 27.9 | ||

Note:

- Gold price used in the first three years of production is

$200 per ounce higher than long-term gold price in economic sensitivity analysis.

Gramalote Project Mineral Resource Estimate

The Mineral Resource estimate for the Gramalote Project has an effective date of December 31, 2023, and is reported using a gold price of

Indicated Mineral Resource Estimate

| Category | Tonnes | Gold Grade (g/t) | Contained Gold Ounces |

| Total Indicated Resources | 192,220 | 0.68 | 4,210,000 |

Inferred Mineral Resource Estimate

| Category | Tonnes | Gold Grade (g/t) | Contained Gold Ounces |

| Total Inferred Resources | 85,370 | 0.54 | 1,480,000 |

Notes:

- Mineral Resources have been classified using the CIM standards.

- Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability. There is no guarantee that all or any part of the Mineral Resource will be converted into a Mineral Reserve. Inferred Resources are considered too geologically speculative to have mining and economic considerations applied to them that would enable them to be categorized as Mineral Reserves.

- All tonnage, grade and contained metal content estimates have been rounded; rounding may result in apparent summation difference between tonnes, grade and contained metal content.

- The Qualified Person for the Mineral Resource estimate is Andrew Brown, P.Geo., B2Gold’s Vice President, Exploration.

- Mineral Resources assume an open pit mining method and are reported within a conceptual pit based on a gold price of US

$1,850 /oz, metallurgical recovery of 81.7–84% for oxide and 90.9–97.6% for sulphide, selling costs of US$62.04 /oz including royalties and levies, and operating cost estimates of US$2.36 –US$2.61 /t mined (average mining cost), US$5.39 –US$5.47 for oxide, US$8.39 –US$8.49 /t for sulphide processed (processing) and US$2.10 /t processed (general and administrative). - Mineral Resources are reported at cut-off grades of 0.16 g/t Au for oxide and 0.19 g/t Au for sulphide.

Gramalote Project Next Steps

B2Gold plans to commence feasibility work with the goal of completing a feasibility study by mid-2025. Due to the work completed for previous studies, the work remaining to finalize a feasibility study for the updated medium-scale project is not extensive. The main work programs for the feasibility study include geotechnical and environmental site investigations for the processing plant and waste dump footprints, as well as capital and operating cost estimates.

The Gramalote Project will continue to advance resettlement programs, establish coexistence programs for small miners, work on health, safety and environmental projects and continue to work with the government and local communities on social programs.

Due to the desired modifications to the processing plant and infrastructure locations, a Modified Environment Impact Study is required. B2Gold has commenced work on the modifications to the Environment Impact Study and expect it to be completed and submitted shortly following the completion of the feasibility study. If the final economics of the feasibility study are positive and B2Gold makes the decision to develop the Gramalote Project as an open pit gold mine, B2Gold would utilize its proven internal mine construction team to build the mine and mill facilities.

About B2Gold

B2Gold is a low-cost international senior gold producer headquartered in Vancouver, Canada. Founded in 2007, today, B2Gold has operating gold mines in Mali, Namibia and the Philippines, the Goose Project under construction in northern Canada and numerous development and exploration projects in various countries including Mali, Colombia and Finland. B2Gold forecasts total consolidated gold production of between 860,000 and 940,000 ounces in 2024.

Qualified Persons

Bill Lytle, Senior Vice President and Chief Operating Officer, a qualified person under NI 43-101, has approved the scientific and technical information related to operations matters contained in this news release.

Andrew Brown, P. Geo., Vice President, Exploration, a qualified person under NI 43-101, has approved the scientific and technical information related to exploration and mineral resource matters contained in this news release.

ON BEHALF OF B2GOLD CORP.

“Clive T. Johnson”

President and Chief Executive Officer

The Toronto Stock Exchange and NYSE American LLC neither approve nor disapprove the information contained in this news release.

Production results and production guidance presented in this news release reflect total production at the mines B2Gold operates on a

This news release includes certain "forward-looking information" and "forward-looking statements" (collectively "forward-looking statements") within the meaning of applicable Canadian and United States securities legislation, including: projections; outlook; guidance; forecasts; estimates; and other statements regarding future or estimated financial and operational performance, gold production and sales, revenues and cash flows, and capital costs (sustaining and non-sustaining) and operating costs, including projected cash operating costs and AISC, and budgets on a consolidated and mine by mine basis; future or estimated mine life, metal price assumptions, ore grades or sources, gold recovery rates, stripping ratios, throughput, ore processing; statements regarding anticipated exploration, drilling, development, construction, permitting and other activities or achievements of B2Gold; and including, without limitation: remaining well positioned for continued strong operational and financial performance in 2024; projected gold production, cash operating costs and AISC on a consolidated and mine by mine basis in 2024; total consolidated gold production of between 860,000 and 940,000 ounces (including 40,000 to 50,000 attributable ounces from Calibre Mining Corp. (“Calibre”)) in 2024; the results and estimates in the Gramalote PEA, including the project life, average annual gold production, total gold production, processing rate, capital cost, net present value, after-tax net cash flow and payback; the potential to convert existing inferred resources to the indicated category; the timing to complete a feasibility study on the Gramalote Project; the completion and results of a feasibility study on the Gramalote Project; receipt of a final approved Modified Environment Impact Study; the potential to develop the Gramalote Project as an open pit gold mine; and B2Gold's attributable share of Calibre's production. All statements in this news release that address events or developments that we expect to occur in the future are forward-looking statements. Forward-looking statements are statements that are not historical facts and are generally, although not always, identified by words such as "expect", "plan", "anticipate", "project", "target", "potential", "schedule", "forecast", "budget", "estimate", "intend" or "believe" and similar expressions or their negative connotations, or that events or conditions "will", "would", "may", "could", "should" or "might" occur. All such forward-looking statements are based on the opinions and estimates of management as of the date such statements are made.

Forward-looking statements necessarily involve assumptions, risks and uncertainties, certain of which are beyond B2Gold's control, including risks associated with or related to: the volatility of metal prices and B2Gold's common shares; changes in tax laws; the dangers inherent in exploration, development and mining activities; the uncertainty of reserve and resource estimates; not achieving production, cost or other estimates; actual production, development plans and costs differing materially from the estimates in B2Gold's feasibility and other studies; the ability to obtain and maintain any necessary permits, consents or authorizations required for mining activities; environmental regulations or hazards and compliance with complex regulations associated with mining activities; climate change and climate change regulations; the ability to replace mineral reserves and identify acquisition opportunities; the unknown liabilities of companies acquired by B2Gold; the ability to successfully integrate new acquisitions; fluctuations in exchange rates; the availability of financing; financing and debt activities, including potential restrictions imposed on B2Gold's operations as a result thereof and the ability to generate sufficient cash flows; operations in foreign and developing countries and the compliance with foreign laws, including those associated with operations in Mali, Namibia, the Philippines and Colombia and including risks related to changes in foreign laws and changing policies related to mining and local ownership requirements or resource nationalization generally; remote operations and the availability of adequate infrastructure; fluctuations in price and availability of energy and other inputs necessary for mining operations; shortages or cost increases in necessary equipment, supplies and labour; regulatory, political and country risks, including local instability or acts of terrorism and the effects thereof; the reliance upon contractors, third parties and joint venture partners; the lack of sole decision-making authority related to Filminera Resources Corporation, which owns the Masbate Project; challenges to title or surface rights; the dependence on key personnel and the ability to attract and retain skilled personnel; the risk of an uninsurable or uninsured loss; adverse climate and weather conditions; litigation risk; competition with other mining companies; community support for B2Gold's operations, including risks related to strikes and the halting of such operations from time to time; conflicts with small scale miners; failures of information systems or information security threats; the ability to maintain adequate internal controls over financial reporting as required by law, including Section 404 of the Sarbanes-Oxley Act; compliance with anti-corruption laws, and sanctions or other similar measures; social media and B2Gold's reputation; risks affecting Calibre having an impact on the value of the Company's investment in Calibre, and potential dilution of our equity interest in Calibre; as well as other factors identified and as described in more detail under the heading "Risk Factors" in B2Gold's most recent Annual Information Form, B2Gold's current Form 40-F Annual Report and B2Gold's other filings with Canadian securities regulators and the U.S. Securities and Exchange Commission (the "SEC"), which may be viewed at www.sedar.com and www.sec.gov, respectively (the "Websites"). The list is not exhaustive of the factors that may affect B2Gold's forward-looking statements.

B2Gold's forward-looking statements are based on the applicable assumptions and factors management considers reasonable as of the date hereof, based on the information available to management at such time. These assumptions and factors include, but are not limited to, assumptions and factors related to B2Gold's ability to carry on current and future operations, including: development and exploration activities; the timing, extent, duration and economic viability of such operations, including any mineral resources or reserves identified thereby; the accuracy and reliability of estimates, projections, forecasts, studies and assessments; B2Gold's ability to meet or achieve estimates, projections and forecasts; the availability and cost of inputs; the price and market for outputs, including gold; foreign exchange rates; taxation levels; the timely receipt of necessary approvals or permits; the ability to meet current and future obligations; the ability to obtain timely financing on reasonable terms when required; the current and future social, economic and political conditions; and other assumptions and factors generally associated with the mining industry.

B2Gold's forward-looking statements are based on the opinions and estimates of management and reflect their current expectations regarding future events and operating performance and speak only as of the date hereof. B2Gold does not assume any obligation to update forward-looking statements if circumstances or management's beliefs, expectations or opinions should change other than as required by applicable law. There can be no assurance that forward-looking statements will prove to be accurate, and actual results, performance or achievements could differ materially from those expressed in, or implied by, these forward-looking statements. Accordingly, no assurance can be given that any events anticipated by the forward-looking statements will transpire or occur, or if any of them do, what benefits or liabilities B2Gold will derive therefrom. For the reasons set forth above, undue reliance should not be placed on forward-looking statements.

Non-IFRS Measures

This news release includes certain terms or performance measures commonly used in the mining industry that are not defined under International Financial Reporting Standards ("IFRS"), including "cash operating costs" and "all-in sustaining costs" (or "AISC"). Non-IFRS measures do not have any standardized meaning prescribed under IFRS, and therefore they may not be comparable to similar measures employed by other companies. The data presented is intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS and should be read in conjunction with B2Gold's consolidated financial statements. Readers should refer to B2Gold's Management Discussion and Analysis, available on the Websites, under the heading "Non-IFRS Measures" for a more detailed discussion of how B2Gold calculates certain of such measures and a reconciliation of certain measures to IFRS terms.

Cautionary Statement Regarding Mineral Reserve and Resource Estimates

The disclosure in this news release was prepared in accordance with Canadian National Instrument 43-101, which differs significantly from the requirements of the United States Securities and Exchange Commission ("SEC"), and resource and reserve information contained or referenced in this news release may not be comparable to similar information disclosed by public companies subject to the technical disclosure requirements of the SEC. Historical results or feasibility models presented herein are not guarantees or expectations of future performance.