Verisk (Nasdaq: VRSK) with APCIA reports a stronger U.S. property/casualty industry through Q3 2025, driven by premium growth and reduced extreme weather losses. Key metrics: $35.3B underwriting gain, 94% combined ratio, net written premiums of $740.7B, and policyholders' surplus of $1.20T.

Realized capital gains fell to $15.6B, and figures cover ~97.9% of U.S. P/C business written.

Loading...

Loading translation...

Positive

Underwriting gain of $35.3 billion through nine months of 2025

Combined ratio improved to 94%, first sub-95 through Q3 in a decade

Net written premiums rose 5.1% to $740.7 billion

Policyholders' surplus increased to $1.20 trillion

Negative

Realized capital gains dropped to $15.6 billion from $75.5 billion year-earlier

Mid-year incurred losses and LAE increased 5.4% at June 30, 2025

News Market Reaction – VRSK

-3.02%

-3.02%Session close to close

In the Feb 6 session, VRSK declined 3.02%, reflecting a moderate negative market reaction.

This announcement underscores strengthening U.S. property/casualty industry fundamentals, including ...

Analysis

This announcement underscores strengthening U.S. property/casualty industry fundamentals, including a $35.3 billion underwriting gain, a 94 percent combined ratio, and policyholders’ surplus rising to $1.20 trillion. For Verisk, it reinforces the relevance of its analytics in an environment of improved pricing and moderated catastrophe losses. In context of recent strategic divestitures, collaboration deals, and prior volatile reactions to catastrophe modeling news, investors may watch upcoming earnings and further industry data for how demand and pricing trends translate into Verisk’s own results.

Key Figures

Underwriting gain (9M 2025):$35.3 billionCombined ratio:94 percentNet written premiums:$740.7 billion+5 more

8 metrics

Underwriting gain (9M 2025)$35.3 billionU.S. P/C insurance industry net underwriting gain through first nine months 2025

Combined ratio94 percentU.S. P/C industry combined ratio through first nine months 2025, down from 97.9 percent

Net written premiums$740.7 billionFirst nine months 2025, up 5.1 percent from $704.8 billion in 2024

Net earned premiums$711.2 billionFirst nine months 2025, up 6.9 percent from $665.5 billion in 2024

Policyholders’ surplus$1.20 trillionU.S. P/C policyholders’ surplus vs $1.12 trillion in same 2024 period

Realized capital gains$15.6 billionU.S. P/C realized capital gains, down from $75.5 billion in 2024 period

Underwriting gain (1H 2025)$11.6 billionFinalized underwriting gain for first six months 2025 vs $3.8 billion prior year

Incurred loss growth0.6 percentIncrease in incurred losses and LAE through nine months 2025 vs 2.7 percent in 2024

Expanded KYND collaboration to add cyber risk intelligence to Rulebook platform.

24h Move is the share-price change in the day after each event; other market factors may also have contributed.

Pattern Detected

Recent headlines show mixed but often negative next-day reactions, including a -10.11% move on an insured-loss estimate and smaller moves around strategic and collaboration news.

Recent Company History

Over the last few months, Verisk news has centered on industry analytics, strategic portfolio shaping, and capital allocation. On Dec 10, 2025, it expanded a cyber-risk collaboration, followed by ending the AccuLynx acquisition on Dec 29, 2025 and selling its Marketing Solutions business on Jan 8, 2026 to focus on global insurance data and analytics. A winter storm loss estimate on Feb 3, 2026 drew a sharp negative reaction. Today’s industry report reinforces Verisk’s positioning as a key data and analytics provider to property/casualty insurers.

Key Terms

underwriting gain, combined ratio, incurred losses, loss adjustment expenses, +4 more

8 terms

underwriting gainfinancial

"factors contributing to a $35.3 billion underwriting gain."

Underwriting gain is the profit an insurance business makes from its core activity of taking on risk—calculated as the premiums it collects minus the claims it pays and the direct costs of writing policies. Think of it like a shop selling warranties: if the money taken in for warranties exceeds what the shop pays out to fix products and the cost of selling the warranties, that surplus is the underwriting gain. For investors, a consistent underwriting gain shows that an insurer’s pricing and risk selection are sound and not being propped up by investment returns, making the company’s core business more sustainable.

combined ratiofinancial

"The combined ratio improved to 94 percent, down from 97.9 percent"

The combined ratio is a way insurance companies measure how well they are doing by adding up all their costs and claims and comparing them to the money they earn from premiums. If the ratio is below 100%, it means the company is making a profit; if it's above 100%, they are losing money. It helps see if an insurance company is financially healthy or not.

incurred lossesfinancial

"Incurred losses and loss adjustment expenses increased just 0.6 percent"

Incurred losses are financial setbacks a company has already suffered during a reporting period — losses from bad loans, write-downs, legal settlements or other events that have happened even if cash hasn’t yet changed hands. Investors care because these losses reduce reported profits and may signal weaker future cash flow or the need for bigger reserves, much like a homeowner recognizing repair costs that will lower their available savings.

loss adjustment expensesfinancial

"Incurred losses and loss adjustment expenses increased just 0.6 percent"

Costs an insurance company incurs to investigate, process, defend and settle claims — for example, fees for claims adjusters, legal defense, and settlement negotiations. These expenses act like the labor and admin needed to handle a warranty repair: they don’t pay the claim itself but add to the total cost of claims, so rising loss adjustment expenses reduce insurers’ profits and signal how efficiently future claims are likely to be handled.

policyholders’ surplusfinancial

"Policyholders’ surplus increased to $1.20 trillion from $1.12 trillion"

Policyholders’ surplus is an insurance company’s financial buffer — essentially its assets minus its liabilities — that represents the money available to pay unexpected claims and absorb losses. Investors watch this number because a larger surplus means the insurer is better able to cover claim shocks, write new policies and meet regulatory tests; it’s like a rainy-day fund that shows how safely the business can operate and grow.

realized capital gainsfinancial

"Realized capital gains continued to decline to $15.6 billion"

Realized capital gains are the profits an investor actually locks in when they sell an asset for more than they paid, as opposed to gains that only exist on paper while the asset is still owned. They matter because they change an investor’s cash position and tax bill—like cashing in a collectible that raises your pocket money and may trigger a tax payment—and they directly affect reported investment returns and available funds for reinvestment or dividends.

reinsurersfinancial

"including reinsurers, excess and surplus insurers, and domestic insurers"

Reinsurers are companies that sell insurance to other insurance companies, taking on part of their losses so the original insurers are less exposed to big claims. For investors this matters because reinsurers help prevent a single large disaster from wiping out an insurer’s finances, influence industry pricing and profitability, and can themselves be sensitive to catastrophic events and capital needs—think of them as a backup safety net for insurance firms.

residual market insurersfinancial

"excluding state funds for workers' compensation and other residual market insurers"

Residual market insurers are the organizations or state-run pools that provide insurance when private companies won’t cover a risk—think of them as the safety net for customers who can’t find coverage on the open market. They matter to investors because these carriers concentrate harder-to-place, often higher-cost policies and operate under special rules that can affect premium rates, insurer assessments, and potential losses that ripple across the broader insurance industry.

Verisk and APCIA report $35.3 billion underwriting gain through first nine months of 2025; combined ratio improves to 94 percent

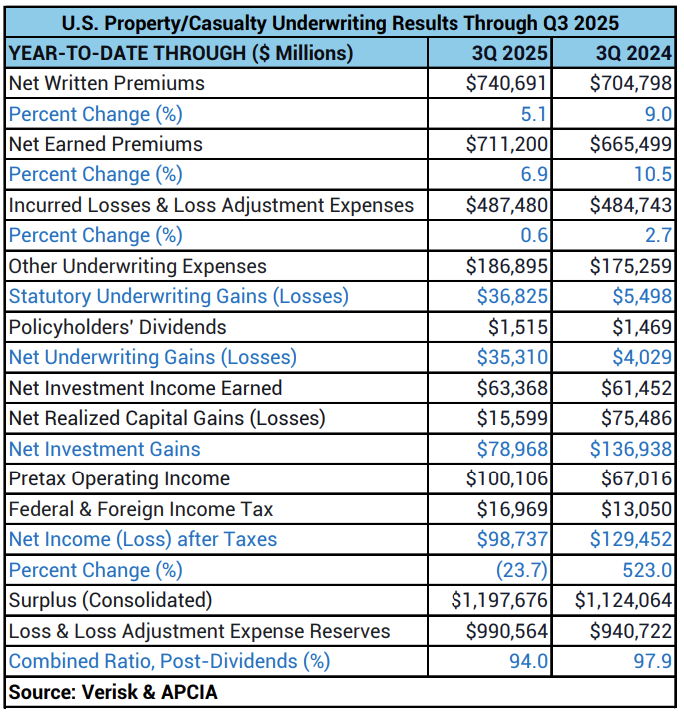

JERSEY CITY, N.J., Feb. 06, 2026 (GLOBE NEWSWIRE) -- Verisk (Nasdaq: VRSK), a leading strategic data analytics and technology partner to the global insurance industry, and the American Property Casualty Insurance Association (APCIA), the primary national trade association for home, auto and business insurers, today announced improvements in U.S. industry performance through the first nine months of 2025. Continued premium growth and reduced extreme weather losses were among the factors contributing to a $35.3 billion underwriting gain.

Underwriting Results Through Third Quarter 2025

Written premiums: Net written premiums grew 5.1 percent to $740.7 billion, compared to $704.8 billion during the same period in 2024. This increase reflects a shift toward adequate pricing and stable demand across most commercial and personal lines.

Earned premiums: Net earned premiums rose 6.9 percent to $711.2 billion, compared to $665.5 billion in 2024.

Underwriting gain: The U.S. insurance industry posted an estimated net underwriting gain of $35.3 billion, a sharp improvement over the $4 billion gain through the first nine months of 2024.

Incurred losses and loss adjustment expenses: Incurred losses and loss adjustment expenses increased just 0.6 percent, compared to a 2.7 percent rise in 2024. The combined ratio improved to 94 percent, down from 97.9 percent from the same time last year. This marks the first time in a decade that the combined ratio has fallen below 95 through the third quarter, signaling stronger underwriting performance.

Surplus: Policyholders’ surplus increased to $1.20 trillion from $1.12 trillion during the same period in 2024.

Realized capital gains: Realized capital gains continued to decline to $15.6 billion, compared to $75.5 billion during the same period in 2024. Adjusting for the capital gains realized by one insurer in 2024, overall investment gains were stable during this period.

Note: The results above are based on annual statements filed with insurance regulators by private property/casualty insurers domiciled in the United States, including reinsurers, excess and surplus insurers, and domestic insurers owned by foreign parents, and excluding state funds for workers' compensation and other residual market insurers, the National Flood Insurance Program, and foreign insurers. The figures are consolidated estimates based on reports accounting for about 97.9 percent of all business written by U.S. property/casualty insurers. All figures are net of reinsurance unless otherwise noted and occasionally may not balance due to rounding.

2025 Mid-Year Adjustments

Following adjustments to previously reported first-half results, underwriting gains for the first six months of 2025 were finalized at $11.6 billion, up from a $3.8 billion gain in the prior year. Insurers wrote $489 billion in premiums during the first half, reflecting a slowdown in growth to 5.4 percent. Earned premiums grew 7.4 percent to $469 billion. Incurred losses and loss adjustment expenses increased by 5.4 percent, compared to a 2.4 percent increase at mid-year 2024. Lastly, policyholders’ surplus rose to $1.13 trillion from $1.07 trillion, as reported mid-year 2024.

Verisk’s Underwriting & Rating Solutions helps global insurers, reinsurers and other stakeholders modernize their processes, reduce operating costs and underwrite risks quickly and precisely. These solutions support (re)insurers across multiple lines of business, including personal & commercial property, personal & commercial auto, small commercial and general liability programming to streamline forms, rules, loss costs and rating-related information.

###

About Verisk Verisk (Nasdaq: VRSK) is a leading strategic data analytics and technology partner to the global insurance industry. It empowers clients to strengthen operating efficiency, improve underwriting and claims outcomes, combat fraud and make informed decisions about global risks, including climate change, catastrophic events, sustainability and political issues. Through advanced data analytics, software, scientific research and deep industry knowledge, Verisk helps build global resilience for individuals, communities and businesses. With teams across more than 20 countries, Verisk consistently earns certification by Great Place to Work and fosters an inclusive culture where all team members feel they belong. For more, visit Verisk.com and the Verisk Newsroom.

About APCIA The American Property Casualty Insurance Association (APCIA) is the primary national trade association for home, auto, and business insurers. APCIA promotes and protects the viability of private competition for the benefit of consumers and insurers, with a legacy dating back 150 years. APCIA members represent all sizes, structures, and regions protecting families, communities, and businesses in the U.S. and across the globe.

Morgan Hurley

Verisk

551-655-7858

morgan.hurley@verisk.com

FAQ

What drove Verisk/APCIA's reported $35.3B underwriting gain through Q3 2025 for VRSK?

The underwriting gain was driven by premium growth and lower extreme weather losses. According to Verisk, net written premiums rose 5.1% while reduced catastrophe losses and pricing strength improved underwriting margins through nine months of 2025.

How did the combined ratio of 94% affect insurer profitability in Q3 2025 for VRSK-related industry data?

A 94% combined ratio indicates underwriting profitability for the industry through Q3 2025. According to Verisk, this marks the first time in a decade the ratio fell below 95, reflecting stronger underwriting and lower loss severity year-to-date.

What happened to investment gains in the Verisk/APCIA Q3 2025 report for VRSK investors?

Realized capital gains declined sharply to $15.6 billion year-to-date. According to Verisk, the drop from $75.5 billion in 2024 was concentrated in one insurer's 2024 gains, leaving underlying investment results otherwise stable.

How large is industry premium growth reported by Verisk/APCIA through the first nine months of 2025 (VRSK)?

Net written premiums grew 5.1% to $740.7 billion through Q3 2025. According to Verisk, earned premiums rose 6.9% to $711.2 billion, reflecting pricing adequacy and steady demand across most commercial and personal lines.

What does the increase in policyholders' surplus to $1.20T mean for VRSK investors?

Higher policyholders' surplus indicates stronger insurer balance sheets and capacity for underwriting. According to Verisk, surplus rose from $1.12 trillion to $1.20 trillion year-over-year, supporting resilience against future underwriting and catastrophe risk.