Strong 2025 Underwriting Income Masks Persistent Property/Casualty Insurance Pressures

Rhea-AI Summary

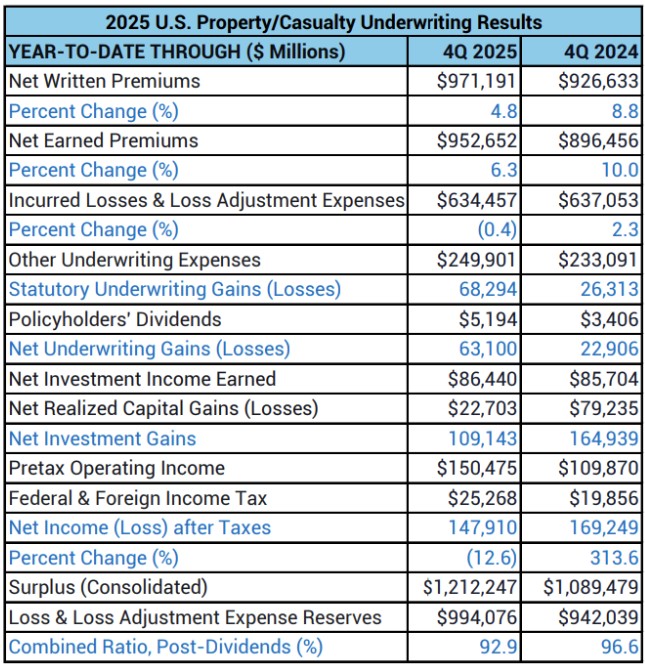

Verisk (Nasdaq: VRSK) and APCIA reported that U.S. property/casualty insurers posted an estimated $63 billion net underwriting gain for 2025, driven largely by unusually low catastrophe losses.

Key metrics: net written premiums $971 billion (+4.8%), combined ratio 92.9%, policyholders’ surplus $1.2 trillion, and net income $148 billion.

Positive

- Underwriting gain $63B for 2025

- Combined ratio 92.9%, improved from 96.6%

- Net written premiums $971B, up 4.8%

Negative

- Net income down $21B (12.6%) to $148B

- Realized capital gains fell to $23B from $79B

- Commercial liability and legal system abuse remain material headwinds

News Market Reaction – VRSK

In the Mar 25 session, VRSK declined 4.97%, reflecting a moderate negative market reaction. Argus tracked a trough of -2.0% from its starting point during tracking. Our momentum scanner triggered 26 alerts that day, indicating elevated trading interest and price volatility.

Data tracked by StockTitan Argus on the day of publication.

Key Figures

Historical Context

| Date | Event | Sentiment | 24h Move | Catalyst |

|---|---|---|---|---|

| Mar 23 | Industry conference | Neutral | -0.9% | Verisk hosts insurance conference focused on risk, data and responsible AI. |

| Mar 17 | Research release | Neutral | -0.5% | Verisk publishes study on rising AI‑driven insurance fraud trends. |

| Mar 05 | Investor Day targets | Positive | -2.0% | Company reiterates multi‑year growth, margin and capital return targets. |

| Feb 23 | Debt offering | Neutral | +5.3% | Pricing of $1.0B senior notes to refinance borrowings and support corporate uses. |

| Feb 23 | Share repurchase | Positive | -0.5% | Company enters $1.5B accelerated share repurchase agreements with two banks. |

24h Move is the share-price change in the day after each event; other market factors may also have contributed.

Recent news often saw muted or negative price reactions, even to seemingly positive strategic updates and capital return actions, with one strong upside move on a debt offering.

Over the past month, VRSK highlighted strategic positioning and capital structure moves. An Investor Day on Mar 5 reiterated medium‑term growth and margin targets, yet shares fell. A $1.5 billion accelerated share repurchase and related debt financing around Feb 23 drew mixed reactions, including a 5.27% gain following senior note pricing. Subsequent AI‑focused conference and fraud research headlines in March prompted only small negative moves. Against this backdrop, today’s industry‑level underwriting update fits into a pattern of the stock not consistently rallying on ostensibly constructive news.

Key Terms

net underwriting gain financial

combined ratio financial

loss adjustment expenses financial

policyholders’ surplus financial

realized capital gains financial

post-tax financial

AI-generated analysis. How Rhea-AI works. Not financial advice.

Limited catastrophe impacts supported P&C underwriting profitability

JERSEY CITY, N.J., March 25, 2026 (GLOBE NEWSWIRE) -- Today, preliminary U.S. property and casualty (P&C) insurance underwriting results for full year 2025 were released by Verisk (Nasdaq: VRSK), a leading strategic data analytics and technology partner to the global insurance industry, and the American Property Casualty Insurance Association (APCIA), the primary national trade association for home, auto and business insurers.

According to key financial indicators for private U.S. P&C insurers, the industry posted an estimated net underwriting gain of approximately

“The industry delivered one of its strongest underwriting results in years in 2025, supported by a near-record low combined ratio, but that outcome was driven more by unusually low catastrophe losses rather than a fundamental shift in industry risk,” said Saurabh Khemka, president of Verisk Underwriting Solutions. “A near 90 percent decline in hurricane-related claims in 2025 materially reduced catastrophe losses, an improvement that reflects limited U.S. landfall rather than a change in underlying exposure.”

Khemka added: “Still, some lines, including personal auto, showed core improvements following strong rate action and tighter underwriting discipline, while workers’ compensation continued to deliver consistently favorable results. At the same time, overall premium growth decelerated and commercial liability continued to weigh on overall performance. Taken together, these dynamics make 2025 a reset after several years of volatility, not a new normal. Ongoing catastrophe variability, moderating rate momentum and elevated legal system costs mean underwriting discipline remains critical heading into 2026 and beyond. That reality is already playing out this year, as recent tornado and hail events serve as an early reminder of the volatility that continues to define catastrophe risk.”

2025 Full-Year Underwriting Results

- Written premiums: Net written premiums grew 4.8 percent to

$971 billion , compared to$927 billion in 2024. - Earned premiums: Net earned premiums rose 6.3 percent to

$953 billion , compared to$896 billion in 2024. - Underwriting gain: The U.S. insurance industry posted an estimated net underwriting gain of

$63 billion , an improvement over the$23 billion gain in 2024. - Incurred losses and loss adjustment expenses: Incurred losses and loss adjustment expenses decreased 0.4 percent, compared to a 2.3 percent rise in 2024.

- Combined ratio: The combined ratio improved to 92.9 percent, down from 96.6 percent in 2024.

- Surplus: Policyholders’ surplus increased to

$1.2 trillion from$1.1 trillion in 2024. - Realized capital gains: Realized capital gains continued to decline to

$23 billion , compared to$79 billion in 2024. Adjusting for the capital gains realized by one insurer in recent years, overall investment gains were in line with historical averages, although up from 2022 and 2023. - Net income: Net income after taxes declined to

$148 billion from$169 billion in 2024, a$21 billion decline.

“Industry results continued to stabilize in 2025. Incurred losses were largely flat, reflecting the unusual lack of hurricanes making landfall in the United States,” said Robert Gordon, senior vice president, policy, research and international at APCIA. “Consumers benefited from the slow-down in insurance cost-drivers, as net written premium growth slowed from 8.8 percent in 2024 to 4.8 percent. Personal and commercial insurance spending declined in 2025 relative to total consumer spending and gross industrial output, respectively. Insurers’ net income declined by 12.6 percent, partly reflecting reduced realized capital gains. Market performance varied significantly by state and line of business. For example, homeowners and auto insurance losses and rates in Florida in 2025 declined significantly following legal system abuse reform, while loss ratios nationwide for contractor’s liability remained elevated. Legal system abuse continues to challenge commercial liability lines, with significant adverse reserve additions for recent years continuing in commercial auto liability and other liability. While industry premium growth significantly slowed in 2025, particularly in personal lines, losses will continue to face long-term pressures from continuing inflation, demographic shifts, natural disaster severity and legal system abuse.”

Continued pressures on the horizon

Escalating material and labor costs continue to drive higher repair and replacement expenses, particularly for roofs, while underinsurance and rising claim severity complicate loss outcomes, coverage gaps and add pressure to loss costs. At the same time, frequent and intense hail and severe convective storms are expanding exposure beyond traditional geographies. As a result, recent profitability should be viewed against a backdrop of persistent and evolving risk as the industry moves through 2026 and beyond.

Note: The results above are based on annual statements filed with insurance regulators by private property/casualty insurers domiciled in the United States, including reinsurers, excess and surplus insurers, and domestic insurers owned by foreign parents, and excluding state funds for workers' compensation and other residual market insurers, the National Flood Insurance Program, and foreign insurers. The figures are consolidated estimates based on reports accounting for about 97.8 percent of all business written by U.S. property/casualty insurers. All figures are net of reinsurance unless otherwise noted and occasionally may not balance due to rounding. Net investment results displayed are post-tax.

###

About Verisk

Verisk (Nasdaq: VRSK) is a leading strategic data analytics and technology partner to the global insurance industry. It empowers clients to strengthen operating efficiency, improve underwriting and claims outcomes, combat fraud and make informed decisions about global risks, including climate change, catastrophic events, sustainability and political issues. Through advanced data analytics, software, scientific research and deep industry knowledge, Verisk helps build global resilience for individuals, communities and businesses. With teams across more than 20 countries, Verisk consistently earns certification by Great Place to Work. For more, visit Verisk.com and the Verisk Newsroom.

About APCIA

The American Property Casualty Insurance Association (APCIA) is the primary national trade association for home, auto, and business insurers. APCIA promotes and protects the viability of private competition for the benefit of consumers and insurers, with a legacy dating back 150 years. APCIA members represent all sizes, structures, and regions protecting families, communities, and businesses in the U.S. and across the globe.

Morgan Hurley Verisk 551-655-7858 morgan.hurley@verisk.com